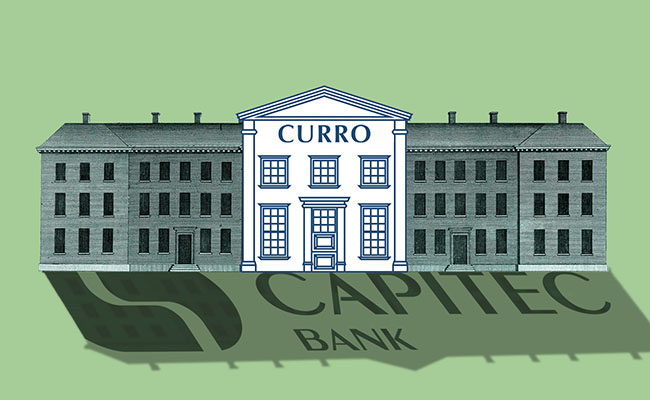

Make no mistake, this is a big transaction. But is it really a massive philanthropic one? The Mouton family’s proposal is that Curro shareholders swop their reasonably unattractive Curro shares for very attractive Capitec shares owned by the Jannie Mouton Foundation (JMF). Curro shareholders will also get a few PSG Financial Services shares and a bit of cash.

In exchange all of Curro will be shifted into the JMF.

There’s little doubt that when the transaction is finalized, the Curro shareholders, including the Mouton family with around 24%, will be sitting with more attractive assets than they were at the start. Who wouldn’t want more Capitec and less Curro?

The JMF will be sitting with something less attractive than it started: 100% of Curro, a company that once held great promise but in recent years has been struggling.

That’s not to say Curro won’t become much more appealing. If management of South Africa’s largest independent school network can take advantage of its status as a PBO (Public Benefit Organisation), most importantly not having to pay dividends or tax, there’s nothing to stop it thriving. South Africa certainly needs it to thrive as it serves an important segment of an extremely important market. And if it does, it should be able to afford much greater numbers of bursaries.

As for the philanthropy, well the major philanthropic event happened years ago – August 2017 to be precise. That was when Jannie Mouton, founder of the PSG group, which included Capitec and Curro, announced he was establishing a foundation with an endowment value of more than R2bn. It’s largely thanks to the Capitec shares in that endowment that the value of the JMF has grown to around R8bn. That is a staggeringly generous amount of money.

Up to now, the philanthropy has been restricted to distributing the dividend income from the shares in the foundation. That distribution is currently around R100m a year and, according to the Mouton family, is dispersed to about 100 organisations.

Now for the shareholder vote

The proposed transaction represents a complete overhaul of that model. JMF is, as it were, going to put all its money in one basket, looking for a big impact in one area. It is a much riskier strategy.

Of course, this all presumes Curro shareholders will back the deal when they vote on it tomorrow. It seems highly unlikely they won’t. Just check the Capitec share price movement to see how enticing it is.

With every day that passes Capitec shares are reaching record new highs. So, there’s very little reason why Curro shareholders will not vote overwhelmingly in support of the R7.2bn offer. Even if the Mouton family abstained from voting their shares, which they’re certainly not obliged to do, it seems a slam-dunk.

As it is, Curro shares have bounced from a near-record low of 830c to their current R13.65 since the deal was first announced in late August. Initially, the offer was valued at R13/share with the plan to pay shareholders a mix of Capitec shares, PSG Financial Services shares and cash. The biggest chunk of the payment – a hefty 79.7% – would comprise Capitec shares.

What the Curro shareholders will now be focusing on is the uptick in the Capitec share price – from the R3649.50 used in the August offer to R4034.58. This increase has inevitably dragged the Curro share along.

PSG Finance shares, which will make up 13.7% of the offer have inched up to R24.63 from the R23.30 value used for the offer.

Essentially, if you have 1 000 Curro shares you will receive 2.84 Capitec shares, 76 PSG Financial Services shares and R86 in cash.

In total, it comes to assets and cash worth R13 403 – at present market prices. But there’s every chance the figure could rise, or maybe fall, before Curro shareholders are actually paid out.

As Curro pointed out in a SENS statement on Monday (28 October) thanks to the rally in Capitec, and less so, PSG Financial Services, the offer now represents a premium of 74% on the R8.13 at which Curro closed the day before it was announced.

There have been a few mumbles of discontent that the R13 does not include any takeover premium on Curro’s net asset value of R12.49. And certainly, the enthusiasts who bought the share at around its all-time high of R58 – reached almost ten years ago in December 2015 – mightn’t be too happy.

Yet for the most part, Curro stock has had a grim few years since the heady days: plunging during 2016, recovering in 2017; slumping to 594c at the start of Covid; staggering back to a high of R13 in February this year before drifting again.

Some analysts reckon the interim results, released in August, would have propelled the share price even lower had it not been for JMF’s offer. That changed everything.

In a note on those numbers, Anchor Capital decided to downgrade its full-year HEPS expectations, to 80.8c a share from previous estimates of 87.8c. Declining student numbers were the primary problem, with higher debtor costs also contributing to the underperformance.

In contrast, ADvTech, the only other listed private education provider, had released an impressive set of results with earnings per share up 16% on the back of strong enrolment growth.

Of course, the two companies do not operate in the same segments of the private education market. Advtech serves both middle- and upper-income families as well as tertiary students whereas Curro is more focused on providing affordable private education from low to upper-middle-income groups. Its consumer cohort is under considerable cost-of-living pressure which explains the fall-off in enrolments and the sharp increase in the credit loss charge.

‘Rescue bid’

So you can see why some have described the offer as a rescue bid for a failing business model.

The shareholder circular doesn’t quite echo that precise sentiment, but it’s close. It essentially states that management was overly focused on generating high returns for shareholders rather than expanding Curro’s network during South Africa’s recent “anaemic economic” growth.

“Given that Curro will become an NPC (not-for-profit company) and PBO going forward, although it will continue to operate with efficiency and expansion, Curro’s growth will be accelerated through reinvestment of its potential surplus to scale its offering faster and further (both through new builds, expansions, acquiring of schools and innovation in education).”

Curro management and the existing board will be “retained for the immediate future following implementation of the proposed transaction”.

In essence Curro will be escaping the vigorous clutches of the shareholder capitalist system and reverting to a more traditional operating system for schools. For Curro the upside is that money pumped out to shareholders every year in the form of dividends – a generous payout ratio of 20% cost R83m in financial 2024 – can in future be invested in growing the business, which includes reducing the debt. In addition, as a PBO, Curro will not have to pay tax which means it has another R35m or so each year to help grow the business.

Yet all of this extra money will be of little use if it turns out a shortage of funds wasn’t Curro’s only problem and that management isn’t able to realise the JMF vision. The shareholder circular describes this vision as “to position Curro as an everlasting independent education institution that uses its funds to build more schools, expand facilities and its education offering and to provide bursaries for study to augment the government’s efforts to provide excellent education to the leaders of tomorrow.”

The Curro shareholders are certainly winners in this transaction. Whether or not a much broader base of South Africans is, will depend on how well Curro realizes founder Jannie Mouton’s philanthropic ambitions.

Top image: Rawpixel/ Currency collage

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.