If you’ve ever looked up what South African CEOs are getting paid, you’ve probably had to scrape your jaw back off the floor. The latest to score big is incoming Woolworths chief executive Sam Ngumeni with his R100m long-term incentive. And that seems positively mean given the R300m that Old Mutual’s new boss, Jurie Strydom, stands to earn if he hits his targets. Both raise the question: why exactly are CEOs making off with such staggering amounts?

There are several arguments, and none really hold up to close scrutiny.

The central tenet is that CEOs get paid out according to how well the company they are steering does; the better the results, the better the payday. This comes in the form of structured incentive packages – usually the promise of a large number of shares to be vested if management can hit certain financial targets. For Ngumeni, this means getting the Woolworths share price from its current R50 up to R100, alongside other targets.

“In theory the longer-term incentive plans are meant to reward sustained performance,” says Salomé Teuteberg of the Labour Research Service. “But in practice, it’s sort of become the main way that executive pay is inflated.”

Talent pipelines

Then there’s the argument of “scarce skills” – the idea that there is a shortage of individuals with the talent or ability to take on high executive positions. Paying them extraordinary amounts is an incentive to secure a CEO for your company in a CEO shortage. This means trying to lure not only executive management from the small South African pool, but trying to attract international management away from more global offerings.

But experts loathe this argument. Asief Mohamed, himself a CEO at Aeon Investment Management, says boards are often swayed by “the fallacy that you need to get executives that compete globally”, and says that in several cases where high-profile international executives have been brought in, “it’s been a failure”.

It is also, he argues, a sign of board failure, “because they all along should have been able to develop a bench of potential people within the company to take over the CEO role”.

Just Share’s inequality analyst, Kwanele Ngogela, shares this scepticism of the limited talent pool, and says the argument “really ignores the role of companies in failing to build internal talent pipelines”.

No correlation between pay and performance

As for the argument that CEO payouts correlate to high performance, this too has been thoroughly debunked. In a study of JSE-listed companies done by the Labour Research Service, Teuteberg found that 41 of the 65 companies studied – in other words, a clear two-thirds – saw CEO pay and profit moving in opposite directions.

When it came to Sasol, Telkom and Cashbuild, for example, company profit fell consistently while CEO pay rose. In only a few rare cases was the inverse true.

“Companies themselves are telling us that they’re remunerating performance, but we can see here that that doesn’t align,” Teuteberg explains. “It suggests that the remuneration committees [are] setting pay using criteria entirely unrelated to financial outcomes.”

“Performance” tends to be measured as much by profit as a company’s share price. And for RECM chair Piet Viljoen, it “doesn’t get much worse than Truworths”.

In the retailer’s case, Michael Mark, who has been Truworths CEO since 1991, has overseen a long-term decline in its shares, which have lost 35% of their value over the past 10 years.

Mark’s pay, however, has only risen, and he has racked up more than R350m in remuneration over the same timeframe.

Then there’s the case of The Foschini Group (TFG), whose share price is down nearly 42% over the past five years. In TFG’s case, either the remuneration policy or implementation report was voted against by shareholders for five years running, to 2025. Nevertheless, TFG CEO Anthony Thunström took home nearly R235m in remuneration over the period.

“If a CEO creates value for shareholders, [they] should be remunerated generously,” Viljoen says. But, he says, “current schemes are generally too complicated to be understood by anyone except those who have the most to gain from gaming them – the executives”.

Finding the culprits

There is a wealth of reasons as to why executives still get paid out millions despite a galling lack of correlation to performance.

Here, several of the experts Currency spoke to mention benchmarking, or what Mohamed calls “the ratchet effect”.

Executive pay is generally benchmarked against peer groups, or other companies competing in the same field. “None of these companies want to position their executives below what serves as the median,” Ngogela explains, linking it to the “scarce skills” argument. So, when one company goes a little higher, all the rest have to follow, creating a never-ending upward drift.

It helps explain why Naspers’s Fabricio Bloisi received a structured incentive package worth more than R1bn in 2025.

Then there’s the issue with the metrics and targets that structure the incentive packages. The experts all agree that many of the targets set for CEOs to reach are not sufficiently stretching, “meaning there’s guaranteed vesting”, says Ngogela.

On top of that, it is common for CEOs to have maximum bonus potential set at between 200% and 300% of their total guaranteed pay, explains Teuteberg.

The question of structure

As far as company metrics go, the complex nature of how incentive packages are structured means it is easy to hide guaranteed payouts or increases.

One investment analyst who asked not to be named says he pulled out of investing in Bidvest due to this very issue.

“Bidvest’s management is rewarded using a metric that leaves out the true costs of acquisitions and capital write-offs, inflating their returns. Management are therefore incentivised to buy companies at high prices, even when those deals don’t create long-term value for shareholders,” he tells Currency.

Rob Lewenson, head of responsible investing at Old Mutual, gives a similar example of the controversial proposal made by Anglo American in December 2025 to alter its remuneration metrics, intending to award incentive bonuses worth R190m to top executives, which would be guaranteed upon the completion of the Teck Resources merger. Shareholders were furious and forced the company to withdraw the proposal.

Dubious incentives

Repeat offenders mentioned by the experts include companies’ remuneration committees, as well as the remuneration consultants they bring in to structure these packages.

The remuneration consultants naturally want to retain their contracts with those who hired them – management – and so are incentivised to balloon packages to satisfy their employers.

Ngogela notes a “limited resolve” among most remuneration committees to stand up to management when it comes to structuring these payouts. The non-executive directors sitting on these committees “are drawn from the very same corporate networks as the executives, creating a closed loop of mutual reinforcement”.

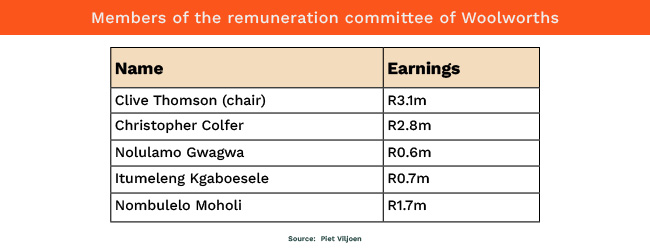

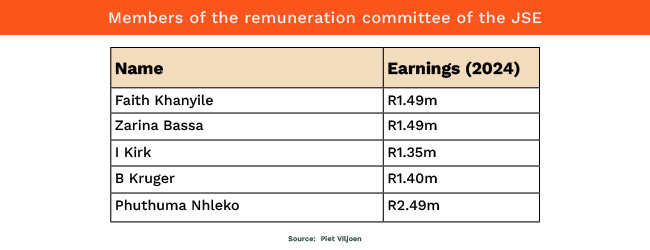

It doesn’t help that they get cushy payouts from management too – Viljoen makes examples of the Woolworths and JSE remuneration committees, whose members have received multimillion-rand payouts for their work.

“Of course, under the King Code, all the members of the remuneration committee are classified as independent directors,” Viljoen says. “But given how much they’re paid, they obviously don’t have the appetite for a heated discussion with management about pay.”

‘Votes don’t matter’

And, ultimately, there’s very little shareholders can do about any of it. Ngogela points back to the TFG example. “Over years and years, investors would vote down the remuneration policy and implementation report, but nothing really changed. Why? Because their votes really don’t matter.”

Because shareholder votes on remuneration policies are advisory, or non-binding, the board and management can simply choose to ignore their votes.

Last year, 61% of shareholders voted against how executives were paid at the Spar Group 2025 AGM, likely stemming from the lump-sum payment of R9.5m awarded to outgoing CFO Mark Godfrey, which was not provided for in the remuneration policy. Nonetheless, Spar went ahead and paid it out.

Mohamed says that when shareholders try to raise their concerns with management, “they’ll argue that you are the first institutional shareholder to raise the remuneration issue. Management is playing the divide and rule game.”

Can shareholders bite back?

Teuteberg advocates for a three-pronged approach to dealing with this problem: regulation, internal changes and more active shareholding.

In terms of regulation, an amendment to the Companies Act has been introduced that would enforce greater transparency via the disclosure of pay ratios in companies, as well as an amendment to make shareholder votes on remuneration policies binding. The experts all think these changes will make a genuine difference, but until they’re implemented, companies can continue to ignore shareholder votes.

Internal changes would include removing jargon from the remuneration policies that companies put out, which are often bafflingly convoluted and unclear.

“Remuneration policies are extremely difficult to understand, and I believe it’s by design,” says Teuteberg. By putting public pressure on firms to simplify their policies, Teuteberg hopes that “once a shareholder understands how pay is structured, then they can bring that issue into AGMs and engage with the company secretary”.

Because, as she points out, “we have extremely passive shareholding in South Africa”. To be able to get shareholders more in tune with what is happening means a more active base that has real power in publicly questioning what CEOs are being paid, and what exactly they are being rewarded for. As Teuteberg says, “are we as a society condoning paying Bloisi a billion rand? I don’t think that we are.”

ALSO READ:

- Behind Jurie Strydom’s R300m bonus

- JSE CEOs: Caviar pay, sardine results

- How rubber-necking execs gamed the JSE’s pay disclosure system

Top image: Rawpixel/Getty/Currency collage.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.