Boringness is an underappreciated facility. You want a boring pilot, for example. And a boring anaesthetist is actually fine. An exciting accountant has three cellphones, a Panama hat and an extradition problem.

In politics, theatricality is at the moment practically a job requirement, and oddly enough, it’s getting to be pretty boring.

A long time ago, Denis Beckett wrote a memorable piece in the magazine Frontline in the midst of the turbulent and violent days just prior to South Africa’s democratic transition. He wrote that he longed to live in a boring country, where nothing of significance ever happened, as opposed to the endless drama of a country in turmoil.

Which brings us, with all the glamour of a beige cardigan, to South Africa’s latest budget.

As editor-in-chief Rob Rose said in the introduction to Currency’s budget coverage newsletter yesterday, for anyone hoping for the eye-popping ructions of last year’s budget – which Enoch Godongwana eventually had to deliver three times – the finance minister’s presentation in parliament couldn’t have been more dull. But it’s not only Godongwana’s presentation; it goes further than that.

Dullsville central

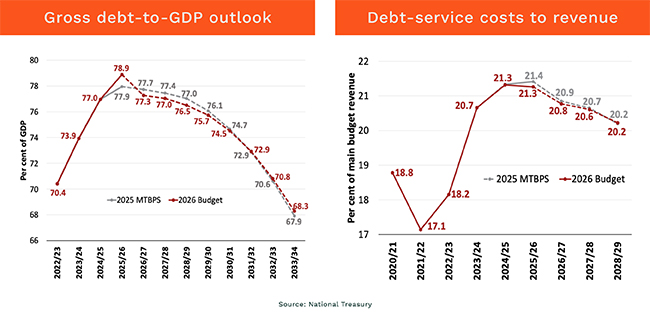

The dullness of the budget is most obviously visible in the absolutely crucial debt-to-GDP level: prior to the publication of the budget, Bloomberg was reporting that consensus was for a one percentage point increase in the debt level to 78% of GDP.

Actually, gross loan debt is budgeted to go higher, at 78.9% of GDP in 2025/26, which is in turn a bit higher than the 77.9% forecast in the medium-term budget policy statement.

Treasury says this is due to changes in the nominal GDP denominator, which means the size of the economy has been calculated to be slightly smaller, which tends to push up the debt-to-GDP proportion.

Still, “stabilisation” is good, and you could call it a “turnaround”, since South Africa’s debt has increased pretty steadily for two decades.

(Though it calls for some cynicism, too, as the Treasury has been predicting debt will decline over a three-year scale – also for almost two decades now).

Look at these numbers: 77.3% to 77% to 76.5%. Of course, we are talking about proportions of a R7.8-trillion economy here, so small percentage changes lead to large absolute numbers. But this is hardly an exciting decline.

And in a sense, that’s the story of the entire budget: stasis.

Incremental innovation

There were a few small innovations, sure: an increase in government spending on infrastructure, which is due to grow more than 20% in the medium term. And an increase in the VAT exemption rate for small business from R1m to R2.3m.

But all of these come with caveats. Government infrastructure spend is not actually a quantity problem; it’s an implementation problem.

For example, the state-owned South African National Roads Agency (Sanral) is actually loaded with cash and has been for years. Sanral’s latest annual report puts its cash balance at a whopping R54bn. It just doesn’t spend it because the construction mafia insist that they get awarded the contracts even when they don’t have the capacity to actually build the road themselves, and the board is packed with people who understand precious little about road construction.

It’s great that the government is at last recognising the utility of small business. But the increase in the VAT exemption level comes after years where it’s been held static. And even the smallest coffee shop in your average mall is probably doing more than R2m a year in turnover. As Leon Louw from the Freedom Foundation keeps telling me, the problem with South Africa’s special economic zones is that they are not special. The VAT exemption for small business falls into the came category.

And then there’s the increase in the annual tax-free savings account allowance, but the retention of the lifetime cap at R500,000. Government claims this is because if you reach a savings level of R500,000, “you are doing okay”. Are they insane? The average length of retirement is around a decade, which means if you retire with R500,000, you have a whole R4,000 a month to spend.

The poverty of small ambitions

And so it goes with lots of other issues. Government just doesn’t want to let go of income, and the result is that it is painfully, irritatingly, horribly unambitious. And that, partly, is why South Africa’s growth rate is “improving” to a tortoise-like 1.6%.

So, yes: the numbers are tidier; the mood is better; the long-term line on the debt graph has stopped resembling a hostage video. But this is not the kind of economic acceleration that makes people feel transformed. It is the kind that allows analysts to use phrases like “constructive and conservative” while ordinary people continue asking whether their salary is moving faster than groceries. This is not champagne. It is flat soda in a clean glass.

Why is it that government finances have become so boring?

I suspect there are three reasons. It’s possible last year’s fiasco has just made the Treasury gun-shy of any grand gesture of any description. And I suspect the new methodology of consulting the government of national unity makes it difficult to move dramatically in a new direction. In a sense, what we are seeing is the tyranny of consensus.

Second, it’s possible debt is now just so large that any increase in income, as was experienced this year, just gets gobbled up by interest payments. The level of interest payments is actually not so much the issue here; there are lots of countries that have much higher debt-to-GDP levels. It’s the combination of high debt levels and high interest rates which is the killer, and is why South Africa will pay R1.2bn a day in interest payments.

The third possibility is that the ANC has just run out of ideas. The party now knows that what it was doing was not getting support from voters and hurting the economy. So, kudos to the ANC, it has retreated from the grand old idea of government “leading” the economy, and everything that this “radical economic transformation” notion implies. But, with the best will in the world, business can’t partner with a dysfunctional corpse, even if it wanted to.

By the battered standards of the age, a boring budget is a modest achievement. Better bland than catastrophic. Better oatmeal than arson.

Yet it is also a slightly mournful one, because what it reveals is how much emotional energy South Africans now expend simply hoping not to be mugged by surprise.

We are not celebrating a feast. We are applauding the waiter for not dropping the soup.

ALSO READ:

- Treasury lifts TFSA limit to R46,000

- 10 things to know about the budget

- South Africa’s debt finally peaks, and growth is the target

Top image: Gallo Images/Jeffrey Abrahams; Rawpixel/Currency collage.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.