South Africa is finally getting a handle on its debt problem – the biggest drain on the government’s ability to deliver services and invest in projects that could lift growth and create jobs.

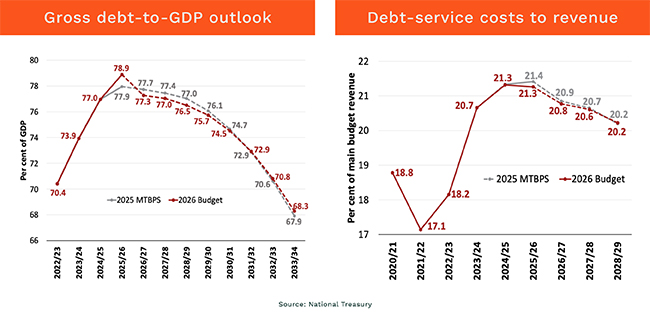

For the first time since the global financial crisis in 2008, when debt stood at about 25% of GDP, Treasury expects debt to peak in the financial year ending March and then begin to fall.

“That period of rising debt has come to an end,” National Treasury director-general Duncan Pieterse wrote in the Budget Review.

The turn is significant, even if the peak is higher than previously forecast. Treasury expects debt to top out at 78.9% of GDP, above last year’s projection in May’s budget of 77.4%, largely because the economy has disappointed (resulting in a lower denominator) and government has issued more debt than planned as it sought to benefit from lower borrowing costs and strong demand.

“Debt consolidation is very much under way,” says Sylvester Kobo, the deputy head of fixed income at Stanlib Asset Management. Those extra bond sales resulted in the government being “overfunded”, which is a “good thing”.

More importantly for the bond market, he says, is that Treasury reduced long-term local debt funding by about R140bn for the 2026/27 fiscal years, as it had built R67bn more cash than planned. This gave it space to cut weekly issuance of nominal bonds by R450m to R2.55bn a week.

“The market did not expect this quantum of issuance cuts and responded positively”, with bond yields falling, Kobo adds. “The last time weekly issuance was at these levels was back in 2018, when debt to GDP was around 50%. We think this adds credence to Treasury’s forecast of debt to GDP dipping below 70% over the next six years.”

Another key pressure point is easing: debt-service costs are now rising more slowly than overall expenditure for the first time this decade.

Since the global financial crisis, South Africa’s debt-service bill has climbed from about 9c of every rand of tax revenue to about 21c; it’s expected to come down to roughly 20c in the 2028/29 financial year. At R432.4bn, it is the single biggest line item in the budget – roughly 20% more than the allocation for basic education, the next-largest category.

Treasury also expects the budget deficit to keep narrowing from an estimated 4.5% of GDP in 2025/26 to 4% in 2026/27 and 3.1% the year after. That helps to stabilise the government’s debt targets as it means less new borrowing, further underpinning the gains seen in bonds.

“South Africa could be back in investment grade within two to three years with at least one of the three big agencies,” says Johann Els, the chief economist at PSG Financial Services, adding that it is a good budget not only for bonds, but shares too. “[The] equity market will like tax relief, stability, [the] improving fiscal situation, impact on confidence and growth.”

Scrapping new taxes

Treasury is also making progress on containing spending. The primary surplus – which excludes interest costs and is a key measure of whether government can stabilise and then reduce debt – is expected to widen to 2.3% over the next three years, from an estimated 0.9% in the year ending March, and 1.6% in the following year.

Treasury described this as the first time since the mid-2000s that government has run a “consistent and growing” primary surplus.

A large part of that improvement comes from a windfall: record gold prices. Treasury said these generated an additional R28bn in revenue. Total revenue is projected at R2.13-trillion, against spending of R2.67-trillion.

That revenue cushion allowed Treasury to scrap R20bn in additional taxes it had pencilled in for this budget.

It also enabled government to adjust personal income tax brackets and medical tax credits by 3.4%, in line with Treasury’s inflation forecast, after two years of no adjustments. Tax-free savings account limits were raised by R10,000 to R46,000 a year. It also increased the maximum retirement contribution and hiked allowances when making gains on the sale of assets. (For more on the savings boost, read our story here.)

“The bracket creep and the overall net effect for cash-strapped consumers for the past two budgets was just compounding the pain that people were feeling in their wallets,” Hayley Parry, the head of education at Worth, tells Currency.

Adjusting that, plus other favourable conditions, such as the lowering of interest rates, “starts to give consumers some breathing room”, she adds, which people should use “towards improving their financial resilience and their financial capability by putting some of that extra money that’s now sitting there into an emergency fund, as an example”.

While there is a feeling by some that the adjustment to personal income tax is too modest, Tertius Troost, director of direct and international taxes at Forvis Mazars, says “it could have been zero … that’s the positive I’m taking away from it because there was a big possibility that they could have just stuck” with the numbers Treasury presented at last year’s budget for no change.

Small business burden lifted

A range of tax limits were lifted to “assist small businesses and encourage savings”, Treasury said.

From April, the compulsory VAT registration threshold rises to R2.3m from R1m – a number that hadn’t been updated since 2009.

Shannon Friedman, the CEO of VAT Modernisation SA, tells Currency that the VAT adjustment for companies will “come as a huge relief to many small businesses just from an administration perspective”. VAT is held by businesses on behalf of the government, so there would little financial benefit from the shift.

There was, however, a miss on the collection side: the South African Revenue Service (Sars) fell R15bn short of its R120bn debt-collection target, after expectations that enforcement could yield an extra R20bn-R50bn.

That was despite R7bn in additional funding to use over the “medium term” to hire 1,500 debt collectors. Treasury said delays in onboarding staff, a rise in disputed debts and more deferred payment arrangements slowed progress. Sars is now working more closely with banks and hiring more legal professionals to pursue civil claims.

Troost points out that Sars should be able to make the shortfall, as this was largely down to delays in appointing staff. The revenue authority’s increasingly aggressive approach “is working”, and as long as it collects what is due “fairly” and avoids “irritating the tax base too much”, “the targets will be met”.

Lukewarm growth projections

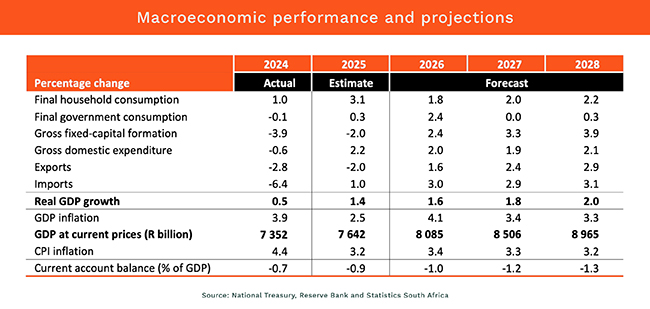

The growth picture is somewhat better – though still underwhelming.

Treasury expects the economy to expand by 1.6% in 2026, compared with an estimated 1.4% last year. At the medium-term budget policy statement in November, Treasury had forecast 1.2%.

Growth could reach 2% by 2028, supported by household spending as inflation eases and real incomes recover. Treasury expects consumer demand to be helped by stronger purchasing power, moderately faster wage growth, wealth gains from higher asset prices, improved consumer sentiment and better credit conditions. It also points to ongoing structural reforms, improved confidence, lower interest rates and higher investment.

In his speech, finance minister Enoch Godongwana flagged persistent logistics bottlenecks, weak public infrastructure and a recent outbreak of foot-and-mouth disease as risks to the economic outlook.

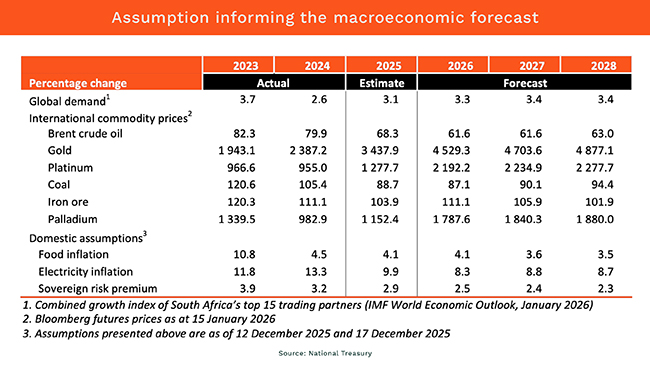

“It is abundantly clear that without a sustained increase in economic growth accompanied by an increase in employment and an improvement in tax morality, the government may struggle to meet its revenue targets,” Stanlib’s Kobo says in a note with chief economist Kevin Lings.

While the government’s initiatives to boost growth “will take time to translate into sustainable higher economic growth”, the “ongoing implementation of the key policy reforms should be combined to lift the growth rate to above 3% over the next three to five years”, they say.

A ‘fiscal anchor’ – without hard numbers

Treasury plans to “entrench” sustainable public finances through a principles-led fiscal anchor, rather than a set of numerical rules, to be developed in consultation with cabinet.

In effect, the fiscal anchor would require each new government to set out upfront how it plans to keep spending within its means – a framework Treasury said will help ensure the public finances remain sustainable.

Asked whether political factions could derail the plan, Godongwana said: “No.”

Municipal overhaul

One of the biggest drags on growth is the decline of local government. Treasury notes that 162 municipalities – 63% of the total – were in financial distress in 2023/24.

Treasury is moving to tighten controls in provinces, including headcount limits and “compensation discipline”. Measures include centralising HR, payroll and administration functions and tightening recruitment approvals.

A clause in the 2026 Division of Revenue Bill will also allow Treasury to redirect infrastructure grants away from municipalities that have “proven incapable of implementation” and towards the Development Bank of Southern Africa, the Municipal Infrastructure Support Agent, or capable district municipalities.

Over the next three years, public sector spending is projected to exceed R1-trillion. Of that, R577.4bn will be spent by state-owned companies and other public entities; R217.8bn by provinces; and R205.7bn by municipalities.

“The fastest-growing item of expenditure is spending on buildings and other fixed structures, which increases by 9.9% over the medium term,” Treasury said. “This reflects a deliberate shift in the composition of spending to infrastructure investment to support service delivery and economic growth.”

Izak Odendaal, an investment strategist at Old Mutual, says the government’s commitment to invest in infrastructure and work more closely with the private sector “demonstrates a clear commitment to boosting South Africa’s long-term economic capacity”, and also has the potential to create jobs. And while it won’t result in any credit upgrades, these remain possible over the next 12-18 months.

“This is not just a relief-focused budget,” he says. “It is also a growth-supportive one.”

This story has been updated with reaction from industry experts.

ALSO READ:

- Treasury lifts TFSA limit to R46,000

- 10 things to know about the budget

- Budget by the numbers: Tax relief and a break for diamond miners

Top image: Finance minister Enoch Godongwana. Picture: Gallo Images/Brenton Geach.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.