Unless the Iran war ends soon, the fuel-price relief granted to motorists this week will feel like an illusion – one that has merely delayed the inevitable pain while complicating the government’s delicate fiscal balancing act.

On Tuesday, National Treasury and the department of mineral and petroleum resources extended a R3/l fuel-levy cut until June 2, with diesel relief widened to R3.93/l from May 6 – zeroing out the diesel levy entirely.

From June 3, the relief halves to R1.50/l for petrol and R1.96/l for diesel. On July 1, it falls away. The general fuel levy returns to R4.10/l for petrol and R3.93/l for diesel.

Finance minister Enoch Godongwana is, in effect, saying this far and no further.

“Treasury is drawing a line in the sand,” Jee-A van der Linde, principal economist at Oxford Economics Africa, tells Currency. The minister has to weigh fiscal-consolidation targets against consumer pain, he says, and providing support regardless of the cost would risk rattling markets.

Godongwana made it clear from the start that the relief was always going to be “limited”. The R17.2bn in revenue that government will forgo will be recouped through higher-than-expected tax collections and underspending – protecting Treasury’s credibility with lenders, ratings agencies, and investors after the budget’s promises to stabilise finances and lower the debt-to-GDP ratio.

Credibility at stake

But a second institution’s credibility is also at stake: the South African Reserve Bank (SARB). Governor Lesetja Kganyago and his team have to defend their 3% inflation target, with a one-percentage-point tolerance band on either side.

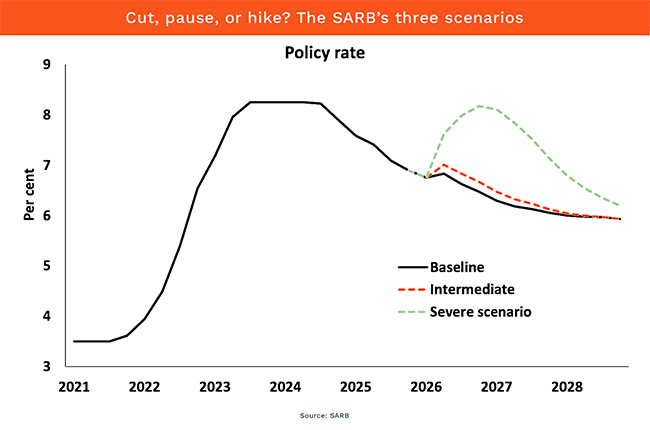

Two months of mercy and a third of grace give the central bank some leeway. What Treasury is trying to head off is the SARB’s severe scenario, sketched out in the latest Monetary Policy Review (MPR) released earlier this month. That is the path in which the Iran conflict drags out for more than a year and Brent crude stays well above $100/barrel. In that case, the SARB warns it may need to front-load hikes that take the repo rate above 8%, from 6.75% now. Prime would push above 11.5%.

The MPR mapped out two other paths. The baseline assumes a contained conflict, with rates easing towards around 6% over the medium term as inflation returns to the 3% target by 2028. The intermediate scenario assumes a short, two-month conflict with stickier oil prices, calling for modest tightening to around 7%.

By absorbing a few rounds of fuel-price shock now, Treasury keeps the baseline path – and eventual rate cuts – alive. Without the cushion, the SARB would likely have been forced down the severe track within weeks.

But South Africa barely has the fiscal space to extend the relief, despite record-breaking tax collection by the South African Revenue Service (Sars), says Chris Hattingh, executive director at the Centre for Risk Analysis. Sars collected R2-trillion for 2025/26, he notes, but “there is no surplus here” once expenditure of more than R2.4-trillion is accounted for.

Manageable vs crisis

The cushion buys consumers only a few weeks of relative stability without changing their underlying exposure, says Hattingh. “For the average motorist, that’s the difference between manageable fuel costs and a genuine budget crisis.” Without the extension, he tells Currency, petrol could have pushed towards R30/l and diesel towards a historic R40/l – figures that would smash into food, transport, and logistics costs.

If consumption comes under significant strain a few months down the line, it “may become the lesser evil to continue providing some support”, Van der Linde believes.

After rebounding to 3.6% in 2025 from 1% in 2024, household consumption – which accounts for about 60% of South Africa’s economy – is expected to slip to 2.3% in 2026 as incomes are squeezed.

That may cause economic growth, which was expected to pick up to 1.4% this year to sink back to just 1%, according to the IMF.

Brent crude has surged from about $75 per barrel before the US and Israel attacked Iran on February 28 to above $110 this week, with Goldman Sachs lifting its fourth-quarter forecast to $90 from $80.

As the conflict has dragged on, Kganyago has become more vocal – warning that the SARB would rather act pre-emptively than deal with inflation after the fact. The strategy paid off during Russia’s invasion of Ukraine, when the SARB and several emerging-market peers moved before developed-market central banks, leaving richer countries to grapple with worse price pressures.

Conundrum

“If you look at the general consensus on oil prices – including our own house view – this is largely seen as a second-quarter shock, with prices easing into the third or fourth quarter,” Van der Linde says. “That’s exactly the conundrum policymakers are facing.”

Treasury does have some room as surging commodity prices bolster its tax take. But monetary and fiscal policy can pull in opposite directions: if Treasury is providing fuel-price support while the SARB is hiking, the policies risk working at cross purposes, Van der Linde warns. That, he says, raises the question of how much value there is in 25 basis-point hikes if Treasury is simultaneously cushioning consumers.

“I’m not saying one approach is right and the other is wrong, but policy coherence is essential in responding to a shock like this. That alignment between fiscal and monetary policy is a critical point.”

Much also depends on the global backdrop. If the US Federal Reserve, which tends to lead the world in the direction of borrowing costs, holds – or if markets begin pricing rate cuts towards year-end – that supports a case for the SARB to stay on hold too.

“To be honest, there’s still a great deal of uncertainty. It’s so hard to commit to a forecast … the situation remains in flux.”

Top image: Per-Anders Pettersson/Getty Images

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.