Most investors ask the same obvious questions when valuing a stock: the company’s growth potential, profit margins or what returns it generates on the money it ploughs into the business. But with Capitec, the sceptics may have missed a trick – they never considered how long the lender could keep beating these metrics.

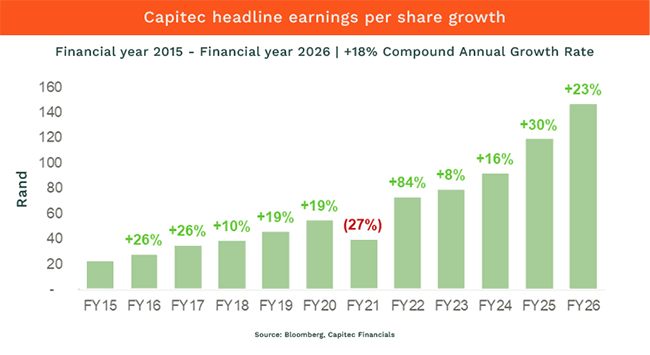

It’s a question worth asking now that Capitec has reported another set of stellar results: return on equity (ROE) clocked in at 31% – way beyond that of any of its rivals – while headline earnings jumped 23%, meaning profit has doubled over the past four years.

The stock has looked expensive for a decade – but it has also jumped almost eightfold over that time, so the doubters have paid for their caution. Still, the share price outperformance overstates Capitec’s lead: the bank pays smaller dividends than its rivals, so the gap between it and the Big Four (by assets) narrows significantly when measured on a total-return basis.

The “how long” question isn’t new. Michael Mauboussin, head of consilient research at Counterpoint Global, a unit of Morgan Stanley Investment Management, calls it the competitive advantage period: the length of time a company can keep earning returns above its cost of capital. It’s the part of every valuation that matters most, he writes in a recent paper titled “The Competitive Advantage Period: The Neglected Value Driver”, yet it gets the least attention.

Stock analysts commonly rely on two methods, both of which are flawed if used in isolation. The first is earnings multiples, which often ignore a firm’s growth dynamics and return on invested capital. Alternatively, they build conventional discounted cash flow models that depend heavily on terminal value – an estimate of the company’s long-term worth that relies on generic formulas rather than its actual competitive strengths.

Ten years ago, any standard model would have heavily understated Capitec’s true value. Even if an analyst correctly forecast the bank’s consistent, double-digit earnings growth, typical financial theory would’ve forced them to anchor the bank’s terminal growth rate to South Africa’s long-term nominal GDP. And, because this single, generic assumption dictates the vast majority of a model’s final output, the formula would’ve artificially dragged down Capitec’s valuation – wrongly signalling to investors that the stock lacked enough upside to buy.

So, in Expectations Investing, the book he co-wrote with Alfred Rappaport, Mauboussin explains what he calls “price-implied expectations analysis”, the process of reverse-engineering a valuation model to gauge the market’s perception of the company’s future performance. Aeon Investment Management’s investment philosophy is built on the same principle, asking what we believe is one of the most important questions: “What’s priced in?”

This analysis helps us answer that question – and the “how long” one posed by Mauboussin, who is also an adjunct professor of finance at Columbia Business School, where he has taught since 1993.

If we apply that logic to Capitec today, his approach suggests the lender can sustain 18% earnings-per-share growth for roughly 10 years. Coincidentally, that is precisely what it delivered over the past decade. Is it plausible that the company can do it again? Well, Bloomberg consensus estimates indicate the growth is possible for the next three years, but far fewer investors would stomach extrapolating it out to 2036.

Why the runway may be longer

Capitec’s structure suggests the runway extends well beyond what the standard assumptions allow.

The bank has 26-million active clients, and non-interest income now accounts for 67%of its income from operations after credit impairments – services that go beyond just lending. Its value-added services and Capitec Connect businesses grew 38% in the 12 months through February and now include cross-border money transfers that span 26 countries. Capitec Connect, South Africa’s largest mobile virtual network operator, grew client volumes 67% in the financial year, giving it 1.5-million active customers.

As its platform continues to add value beyond banking, including other products such as insurance, the runway for excess returns extends. Capitec’s 31% ROE is more than double that of Absa and Nedbank, and more than 10 percentage points ahead of Standard Bank and FirstRand – despite hoarding enormous amounts of lazy capital that could be earning better returns elsewhere.

Having banked the unbanked, Capitec is moving upmarket – making inroads into business banking and partnering with Wise, a global fintech that moves international payments faster and more cheaply than traditional lenders – to segments where legacy banks have long held the advantage.

Investors who underestimated Capitec were not necessarily wrong about near-term earnings. They may simply have been too conservative about how long it could sustain its growth. Companies that maintain excess returns for longer than the market expects – or that break the mould – will always look expensive when assessed on conventional models.

So, the next time a stock has looked overpriced for years, don’t ask what the business earns today. Ask how many more years it can keep earning it.

Shaakir Salie is head of research at Aeon Investment Management, a Cape Town-based boutique asset manager with about R30bn in assets under management.

ALSO READ:

- Why Capitec is miles above the competition

- Inside Capitec’s big bet on fintech

- Why Dis-Chem plans to harness the Capitec juggernaut

Top image collage: Rawpixel; Currency.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.

Nice write up!

great article!