Prior to the SpaceX listing, which as we have been told a zillion times now was the world’s largest IPO, I pugnaciously declared I intended to invest, but fully expected to lose money because the company was plainly and obviously overvalued. Guess what? I actually made money. What does that say about the state of our investment world, and perhaps also my investing prowess?

We’ve known about the “memeification” of stock markets around the world for years now, but the SpaceX listing takes the concept to a whole new level. Despite its size, SpaceX has almost perfect meme-market ingredients: it’s moved by celebrity, community, narrative, social media, retail platforms, options, fractional access and FOMO.

I would love to say – I sneakily hoped this would be the case – that I thought I would make money after all, but in truth I didn’t. I decided to invest because I just thought this is a moment, and we should all embrace the most unusual versions of ourselves.

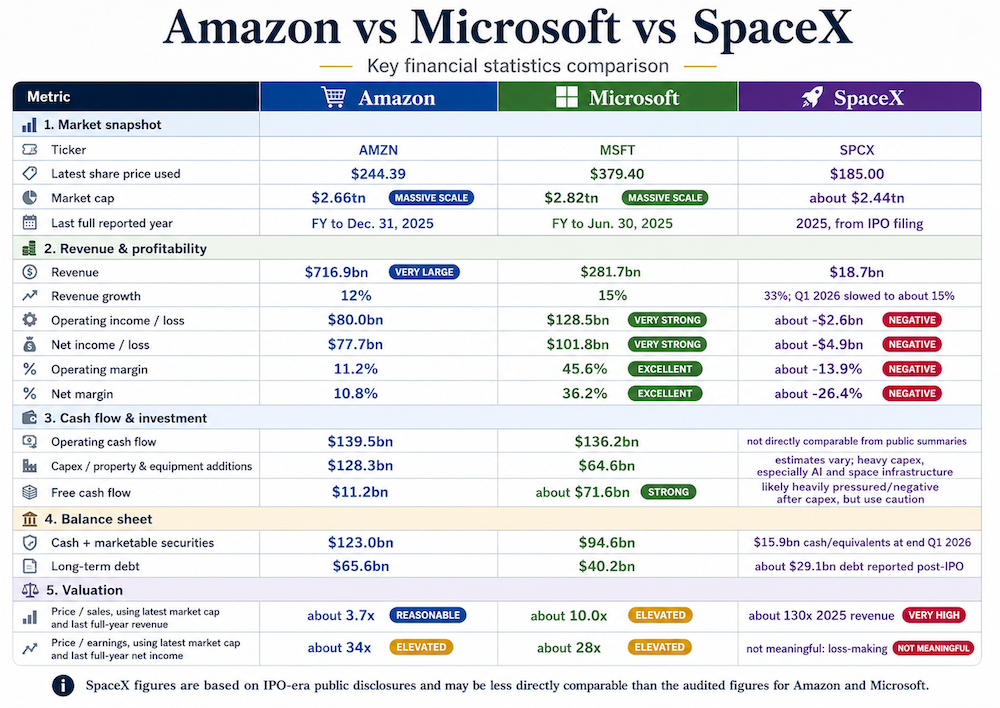

So, it’s with a degree of both embarrassment and satisfaction that I say that, after just over a week of being listed, SpaceX is about 15% up on its listing price and about 37% above the IPO offer price. Its valuation rose as high as $2.97-trillion last week, briefly eclipsing the market value of Amazon and Microsoft of $2.64-trillion and $2.93-trillion, respectively. SpaceX’s market value had fallen back to $2.4-trillion by end of trading on Friday.

Can I just say, in all honesty, this is nuts. SpaceX brought in just $18.67bn in trailing revenue over the past year. At a multiple of 133 times revenue, it would take more than a century of flat revenue just to match its opening valuation. Investors are buying into a grand sci-fi narrative – making humanity multiplanetary, Mars economies, and launching 1-million space-based xAI data centre satellites – rather than cash flows.

Memeification goes mainstream

Obviously, the retail investment market – ergo, investment dolts like me – were key to the listing, and SpaceX knew it, which is why an unusually large 20% of the fairly small available investment book was allocated to retail investors.

Also, major index providers like Nasdaq-100, the MSCI and FTSE Russell waived their mandatory 10% minimum free-float rules and slashed index “seasoning” requirements from three months down to 15 trading days. They did this because leaving a $2-trillion giant out of major indices would cause massive tracking errors for the $16-trillion parked in passive funds, but it does mean that passive asset managers have had to buy in automatically.

In some ways, the proportion of retail investment in SpaceX is the strongest argument in favour of the company becoming the prime example of memeification, and it signifies that memeification of stock markets has gone mainstream. Previously it applied to small stocks like GameStop, Krispy Kreme, Beyond Meat, GoPro, Opendoor and Kohl’s, often driven by social buzz, short interest or catalysts. But with SpaceX that side issue has now become an important market value component.

And that, in turn, reflects the changing nature of stock markets themselves. Pre-2020, retail typically accounted for low-double-digit daily equity trading volume. Post-pandemic, this rose sharply and stabilised at higher levels: estimates range from a 20%-25% average in 2025 (with peaks near 35% in April 2025) to 30%-37% in various adjusted measures. Retail net purchases reached hundreds of billions annually in recent years.

And this is not just the US: the World Economic Forum puts retail at 40% of daily trading volume in India and 80% in China.

Overall, the result is not great, because it pulled the weight of investment towards more immediate returns. Retail volumes can amplify moves via options or sheer volume, as seen in 2021 and echoes since. SpaceX’s early post-IPO swings – surges then drops erasing tens/hundreds of billions in market value – illustrate this dynamic.

A structural change

It should be noted there is a counter-argument that SpaceX is not a meme stock proper, but simply has some meme characteristics.

SpaceX is not a dying mall retailer, a cinema chain or a short-squeeze curiosity. It has real technology, real revenue, real government contracts, Starlink, launch dominance, deep private-market validation and a plausible claim to being one of the most strategically important companies in the world. Calling that memeification risks confusing narrative premium with nonsense.

It might be fairer to say memeification is real in pockets when retail/social forces demonstrably increase short-term volatility and can create self-reinforcing narratives, as vividly shown by SpaceX’s debut. However, it has not memeified the entire stock market. Fundamentals, institutional capital and macro drivers remain foundational. The SpaceX listing blends both: genuine transformative business plus Musk-fuelled retail/social premium and volatility.

Neither was SpaceX’s first-day move wildly outside IPO history. Reuters reported a 19% first-day surge, while Nasdaq’s review of the 2025 IPO market said the average first-day IPO pop in 2025 was 22%, with a median of 13%, and 71% of companies had a positive first-day pop.

The deeper question may be this: the memeification of markets is not about whether the companies are fundamentally distressed (GameStop) or genuinely valuable (SpaceX). It’s about whether price discovery is being crowded out by narrative, mechanics and momentum. On that question, the SpaceX data makes a strong case that, yes, something structural has changed – and it has now reached the very top of the market.

ALSO READ:

- I’m going to buy SpaceX; I’m pretty sure I’ll regret it

- How I learned to stop worrying and love not owning Tesla

- The AI bubble that isn’t quite a bubble yet

Top image collage: Rawpixel; Currency.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.