Once every decade, according to Chen Zhao, chief global strategist and founding partner of Alpine Macro, American markets get themselves into a bubble. It’s almost a constitutional obligation, as though the framers had tucked in a small mischievous clause requiring one act of financial madness per generation. Do we have one now?

In the 1970s it was gold and commodities, in the 1980s Japanese stocks and junk bonds, in the 1990s the internet, in the 2000s housing and commodities, and in the 2010s, when everyone thought they were being terribly sensible, it was government bonds, whose absurdity became visible only when US 10-year Treasury yields fell to about half a percent and then, in 2022, rose from the dead with a baseball bat.

“So all I’m saying,” Zhao told the RMB Think Summit last week, “is this decade we must have a bubble, and the bubble has to be AI. Why? Because it’s written in the US constitution. We have to have one. We will have one.”

Big question. The argument in favour of the US market, and others around the world being in a bubble, is statistically pretty strong. The most technical measure is something called the Shiller CAPE ratio, developed by Nobel laureate economist Robert Shiller and John Campbell. And it was specifically created to answer the question: is a market overvalued or undervalued?

JPMorgan’s latest market guide puts the S&P 500 Shiller CAPE at about 41 times versus a long-run average of 27.2. What’s more, the S&P 500 price-to-book ratio is at 5.6 versus an average of 3.2.

There is another indication: thumping great IPOs.

On June 11 SpaceX hopes to raise $75bn from investors; AI labs Anthropic and OpenAI are likely to be seeking as much as $60bn apiece. Together, the three giga-IPOs may add as much as $4-trillion to the market value of listed American companies in a matter of months.

Companies do not usually rush to list when valuations are miserable, but blockbuster IPOs are often seen as signs that a bull market is nearing its peak. The most extreme example was the 2020/21 listing surge that came just before a bear market. Those earlier IPO booms in the late 1990s and before 2008 were also followed by large slumps.

There are other suggestions too, but these are not quite as clear. The S&P 500 is trading at a forward price-earnings ratio of about 21.2, but that is not much above its five-year average of 19.9 and 10-year average of 18.9, according to FactSet. Analysts are also forecasting a very punchy 22.6% earnings growth for calendar 2026, which means the valuation case depends heavily on those earnings actually arriving.

Always question the obvious

This is usually the stage of the dinner party at which someone reaches for the word “bubble”, drops it into the conversation with the solemnity of a small bomb, and everyone nods because it feels both sophisticated and safe.

Zhao’s argument is that this is precisely the danger.

“When everything becomes so obvious in our business, it is not,” he said. “When everybody thinks that something is so clear, so obvious that it’s going to happen, always question that.”

He began not with Nvidia, OpenAI or the great GPU hoarding operation of our time, but with oil, which is not usually where an AI conversation begins unless someone has taken a wrong turn at a commodities conference. His point was that the world had just been through a familiar cycle of certainty.

At the onset of the latest war-related oil scare, investors and economists rushed to conclude that higher oil prices would inflict serious damage on global growth; Goldman Sachs, Zhao noted with some evident enjoyment, lifted its recession probability sharply. And yet the world economy did something irritating: it refused to co-operate.

Manufacturing data in the US, Europe and China improved at the very moment when the consensus expected deterioration. The reason, Zhao argued, was that the world had changed under everyone’s feet. Oil still matters, but not in the same way. The oil dependency of the US, China and Europe had fallen dramatically over the past quarter century, and in real terms the oil shock was far less severe than the nominal oil price suggested. “What does AI have to do with gasoline prices?” he asked. “Not much.”

Zhao’s broader point was that investors are often most confident when the relevant facts have already been absorbed by the market and when the economy has quietly adapted to the thing everyone is still fearing. The oil scare looked obvious, and therefore it was suspect. The same, he suggested, may now be true of the AI bubble scare.

Punishing underperformance

This may be the best counterargument to Zhao. The argument goes like this: even if AI is real, perhaps especially because AI is real, the market has begun to capitalise not just the profits that exist, but the profits that might exist after a trillion-dollar infrastructure buildout, a reshaping of corporate work, and a wholesale remaking of the software economy. That may happen. It may also happen at returns that do not justify today’s prices. Investors have lost fortunes before by being right about the technology and wrong about the stock.

Zhao did not deny this danger. In fact, he explicitly said the AI bubble will probably arrive. His argument was simply that this is not yet what the evidence shows.

For him, the defining feature of a bubble is not enthusiasm, not large capital spending, not even high valuations in isolation. “Bubble has to be in price,” he said. “And when you’re talking about price, you’re talking about how much you are willing to pay per unit of profits.”

That distinction matters. In the late 1990s, Zhao argued, the US stock market was rising even as corporate profits were already under pressure. Investors were not merely paying high prices for good earnings; they were paying higher and higher prices for companies with little or no earnings at all. “Nobody cared, even though profit actually was contracting,” he said of the internet boom. “The narrative at the time … was that if you have a negative EPS, your stocks usually trade at higher multiples than if you had a positive EPS. If you have negative EPS, you’re investing for the future. If you are profitable … you are stupid.”

Zhao said the current market is behaving very differently. Corporate profits, he said, are still growing strongly, and the market is punishing companies that miss expectations rather than rewarding them for being visionary and loss-making. “If you think about stock market behaviour today,” he said, “any company that underperforms its profit expectation is usually punished severely. People just dump the stocks. So in other words, I think the stock market is still acting very rationally, still very much careful about profits.”

Chip company Broadcom’s recent 15% sell-off is a nice little flare in the night sky: the company still had strong AI chip demand, but its guidance failed to give investors an even bigger sugar rush, triggering a sharp fall.

The market may be expensive, narrow and somewhat excitable, but it has not yet abandoned the profit motive. It’s looking a bit tired, but hasn’t yet gone full Roman banquet.

Don’t confuse a boom and a bubble

Zhao’s second distinction is between a market driven by earnings and one driven by multiple expansion. In the dot-com bubble, stock prices rose because investors were willing to pay more for the same, or worse, profits. Today, he argued, the advance has been far more closely linked to earnings growth.

“This time around the bull market was completely, absolutely, totally driven by profit because there’s no multiple expansion,” he said. “Look at the Nasdaq 100, same story. The p:e ratio actually came slightly down where profit just went through the roof … Back in the 1990s, no profit, but all multiple expansions. That’s a key difference.”

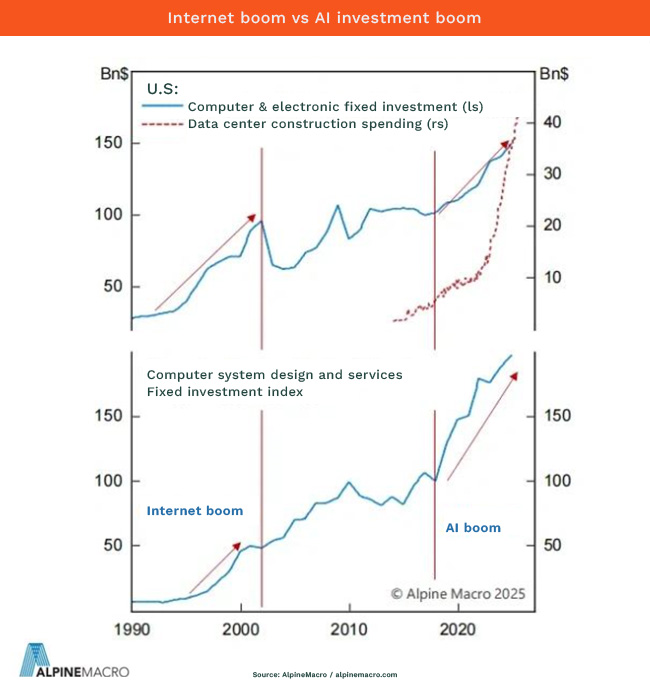

For now, his case is that a boom should not be confused with a bubble simply because it is large, concentrated and noisy. The first half of the internet buildout, as he notes, was real; the madness came later, when legitimate excitement was inflated into a doctrine of permanent exemption from arithmetic. AI may follow the same path, but “may” is doing a lot of work in that sentence.

The market today does have bubble-like features: heroic expectations, magnificent valuations, dangerous concentration and a new-issue calendar that looks as if Wall Street has decided subtlety is for Europeans. But it also has something the late-1990s market increasingly lacked: actual profits growing at actual companies, with actual investors still punishing actual disappointment.

The question is whether we have already crossed from boom into bubble. Zhao’s answer was no: not yet, not while profits are still doing the pulling, not while valuations can still be argued against bond yields, not while disappointment is still punished, and not while the market remains, in his words, “very much careful about profits”.

“The question today is, are we in the bubble or not? That’s the key issue. I don’t think so. I think we’re in the AI boom, but we’re not yet in the bubble. But we will go there.”

The bubble may come. Indeed, if Zhao is right, it almost has an appointment. But his warning to investors is that calling it too early may be another version of the same error he sees everywhere: mistaking the obvious for the truth.

ALSO READ:

- SpaceX: buy the rocket, ignore the smoke?

- Is the AI frenzy today’s new dot-com moment?

- Did the AI bubble pop – and we just didn’t notice?

Top image: Alpine Macro’s Chen Zhao. Picture: StephenC Photography/RMB.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.