At the end of last year, the warnings were everywhere. AI stocks had become the market’s latest bubble; stretched valuations, crowded trades and a narrative running far ahead of reality.

Then 2026 arrived, and the story changed.

Oil surged. Conflict in the Middle East dominated headlines. Investors turned their attention to inflation, interest rates and geopolitical risk. The sense was that the next market shock would come from outside the tech sector.

But while everyone was watching the price of oil, something quieter was happening. The world’s most crowded trade – Big Tech – began to unwind.

Not with a crash. Not with a panic. But with a slow, almost imperceptible reset.

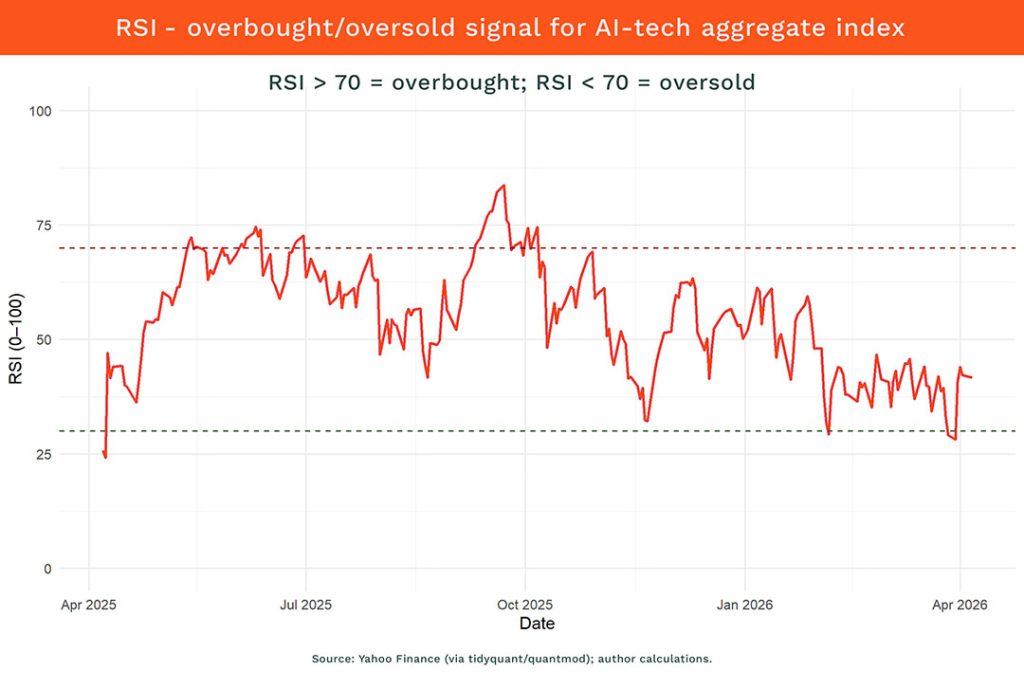

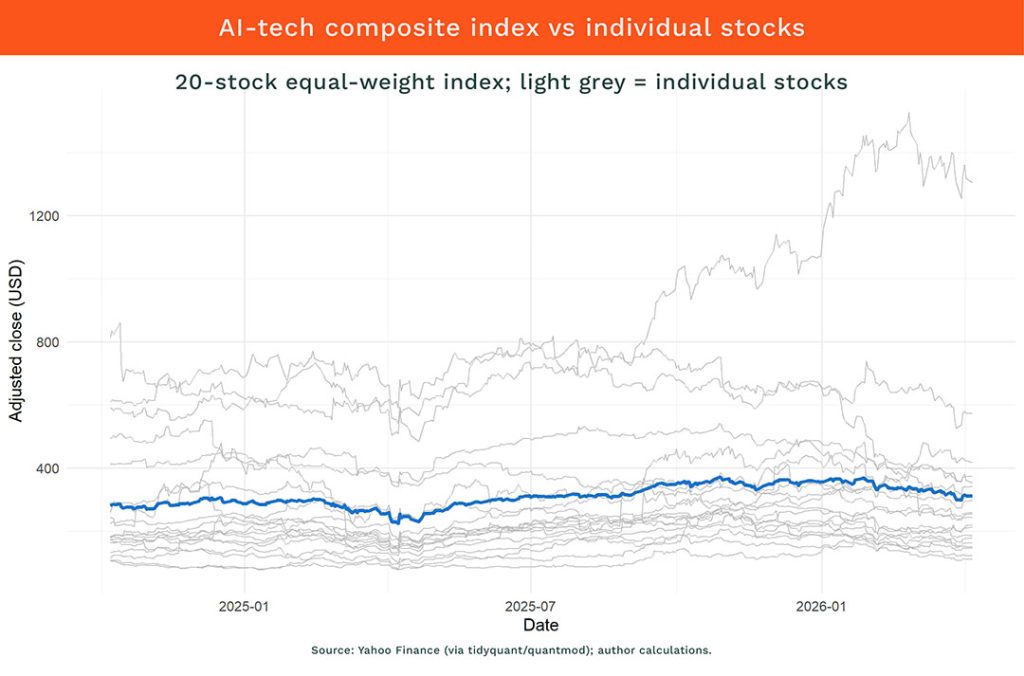

By early April, the 20 largest AI-linked stocks were roughly 15%-20% below their late-2025 peaks. That is not trivial; in market terms, it qualifies as a full correction. Yet it passed with remarkably little comment.

There was no sense of rupture. No defining moment when sentiment broke.

Instead, the decline unfolded gradually, absorbed into the background noise of global events. It is the kind of move that only becomes obvious in hindsight.

This matters because it tells us something important about what the AI trade actually is.

It is not the dot-com bubble.

A complex reality

In 2000, many technology companies had no earnings, little revenue, and business models that depended almost entirely on belief. When sentiment turned, there was nothing underneath to catch prices.

That is not the case today.

The dominant AI firms are among the most profitable companies in history. They generate enormous cash flows and sit at the centre of global digital infrastructure. Their products are real, their demand is real, and their influence on the global economy is substantial.

So if the fundamentals held up, why did prices fall?

The answer lies in expectations.

For much of 2024 and 2025, the AI story was framed as a classic software boom: scalable, high-margin and capable of delivering rapid returns with relatively low incremental cost.

But the reality has proved more complex.

AI is expensive. It requires vast data centres, specialised chips and enormous amounts of electricity. It demands continuous capital investment, not just clever code. In other words, it looks less like pure software and more like a capital-intensive industrial system.

That distinction matters. It changes how investors think about returns, risk and timelines.

Markets have begun to price that in.

Shifting capital

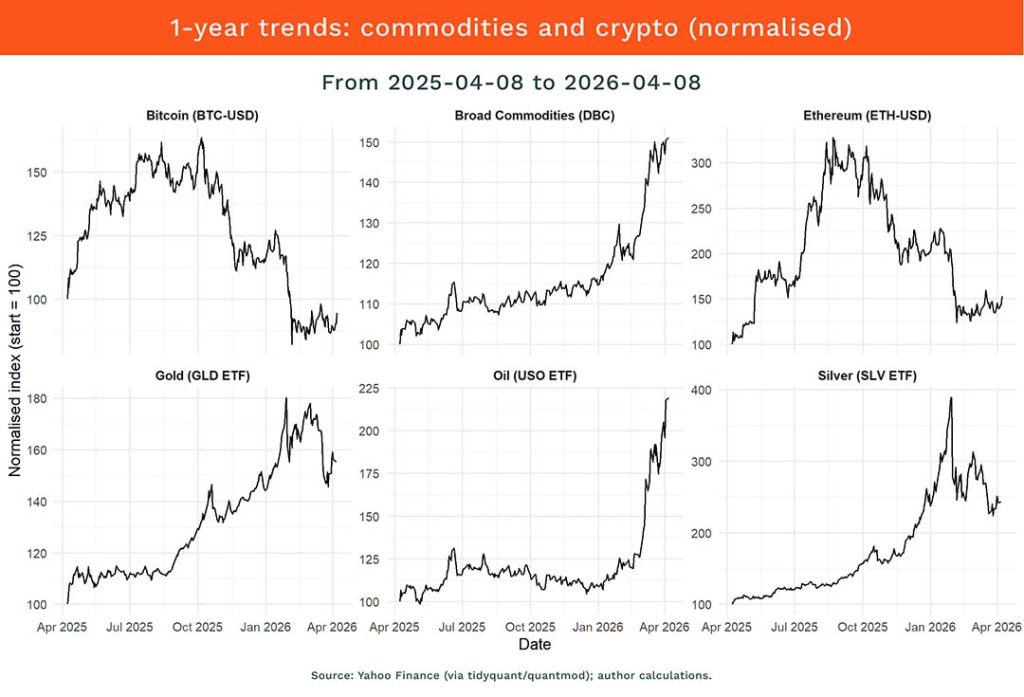

At the same time, geopolitics has provided a convenient distraction.

Rising tensions involving Iran, coupled with higher oil prices, have shifted capital towards energy, commodities and defensive assets. In that environment, technology stocks have often served as a source of liquidity rather than a destination for new investment.

The rotation has been subtle but persistent.

And because earnings have remained strong, there has been no obvious trigger for alarm. Without a collapse in profits, there is no headline moment that forces investors to reassess.

For South Africa, this shift is not as distant as it may seem.

Local pension funds are deeply exposed to global equities, often through index-tracking strategies. Because large US technology firms dominate those indices, even a moderate correction feeds directly into retirement outcomes.

At the same time, the AI build-out is driving demand for energy and metals. That has implications for commodity exporters, including South Africa, particularly in areas such as platinum group metals and manganese.

There is also a currency dimension. Periods of global uncertainty, especially when accompanied by higher oil prices, tend to strengthen the dollar. That, in turn, places pressure on the rand, with knock-on effects for inflation and interest rates.

A slow repricing

So, did the AI bubble burst?

Not quite. The trade did not collapse; it adjusted. Valuations came down, expectations moderated, and the narrative shifted from boundless optimism to something closer to economic reality. In many ways, that is a healthier outcome.

Sharp crashes are easy to spot. Slow repricings are not. Yet it is often these quieter shifts that have the greatest long-term impact, because they change how capital is allocated and what returns can realistically be expected.

The AI story is far from over.

But it has entered a new phase; one where execution matters more than hype, and where the easy gains have likely already been made.

And that is the part that, for now, has gone largely unnoticed.

* For informational purposes only; not investment advice. The author does not knowingly hold direct positions in the securities shown, though exposure may exist via third-party retirement or investment funds.

ALSO READ:

- Are today’s ‘safest’ equity bets tomorrow’s risks?

- Is the AI frenzy today’s new dot-com moment?

- DeepSeek: The algorithm that ate the market

Top image: Rawpixel/Currency collage.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.

Could the slow decline in AI stock valuations represent a healthier market adjustment, or is it an early warning sign of a larger AI investment bubble burst?

How can investors distinguish between genuinely defensive investments and cyclical assets that are only perceived as safe because of current market trends?