On April 2 this year (after local market close) US President Donald Trump announced reciprocal tariffs across most of the US’s trading partners. These were far heavier and more widespread than had been expected, and they sent global markets into a steep fall over the following days. The lowest levels in South Africa were reached on April 7, and on April 9 (again after local market close) Trump announced a 90-day pause, which caused the market to rebound.

This little window provided a mini natural experiment into the behaviour of South African listed property compared to general equities, with the shock across global and local markets relating to risk concerns and growth expectations, and the period being too short for any other fundamentals to impact materially.

In South Africa, the volatility was a little more sustained, as there was significant noise over the period about a possible collapse in the government of national unity – though this dynamic was publicly and financially well in play before Trump’s “Liberation Day”.

A tale of two asset classes

In 2021, David Card, Joshua Angrist and Guido Imbens won the Nobel Prize for Economics – an award that is a not a “real” Nobel, but one established and funded by the Swedish Central Bank in 1968 to mark the bank’s 300th anniversary. It’s called the “Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel”.

This is relevant because the 2021 winners received their award for work that, in some regard, positions economics more as a “proper” science – namely the “natural experiment”. Experiments are hard to conduct in economics, but occasionally you can create two situation that are similar except for some difference in an economic factor. Think of North vs South Korea, or East vs West Germany as “laboratory” experiments.

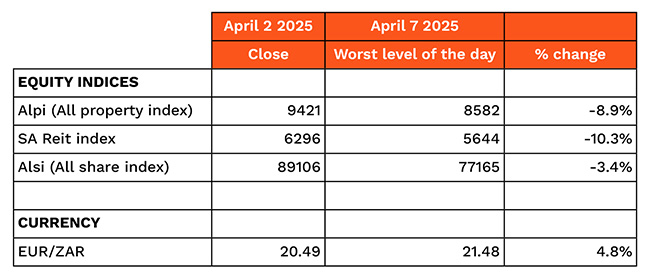

When it comes to our recent natural experiment – involving listed property and equities – we were interested in the extremes. That meant we looked at the movements from the April 2 close, before Trump announced his tariffs, to the very worst intra-day level on April 7. By the time our local markets closed on April 9, before Trump’s announcement that he was pausing tariffs, markets were already well off their worst levels, perhaps in anticipation of some relief.

Factors driving listed property defensiveness

To understand why property is generally more defensive than equities, we need to distinguish between the primary and secondary impacts that usually occur during an economic shock. For listed property companies, when it comes to growth there is often only a modest primary impact from the shock. Real estate investment trusts (Reits) have long-dated contractual leases and this cash flow is not necessarily immediately impacted. The impact comes from secondary effects; some tenants may fail, new tenants may only pay a lower rental rate and lower occupancies with less businesses activity. On the whole, these impacts bleed in over time as leases expire.

In contrast, there would be a primary, direct impact on the profit of, say, a US-based importer or an exporter to the US. Some may not survive. If tariff wars lead to economic hardship, retailers’ sales would immediately fall as a primary impact. These retailers would still need to honour their rental agreements – until these expire and are up for renewal.

Consequently, the predominant contractual cash flows that typically exist in listed property companies should be less negatively impacted than a typical listed company’s non-contractual cash flow. Hence property growth expectations are also affected less. Because economies move in cycles, it means that while listed property is still digesting the secondary impact, a positive growth cycle – or in this example, changes in policy – could be already emerging.

Another factor that’s relevant to the current moment is that property is not export dependent, unlike some (but not all) other industries. Therefore, it should be less negatively impacted in a trade crisis. By contrast, during the Covid outbreak period, South African property was more negatively impacted, as many landlords provided immediate rent relief and therefore took the fall.

Growth expectations are key. When these rise, there is a positive feedback loop. This has implications for the outlook for South African listed property. Listed property fundamentals continue to improve, as we have argued before, and this continues to be evident, though at a slower rate, in recent company results. This improvement may be stymied if the global macroeconomic situation deteriorates, and property as a whole may catch a cold. But it is stable, not weak and sick, as was the case some years ago.

If there is a trade war, confidence-induced recession, or any other growth or risk shock, listed property, as demonstrated, should be more defensive than equities – though not entirely immune – and should provide upside on any positive developments.

For investors looking for an alternative to equities in the current uncertain environment, listed property presents a relative safe haven, as it is not a tradeable sector and should be a beneficiary of any inflationary pressure, should this develop due to trade frictions. South African interest rates are expected to be cut again this year and considering the low level of inflation there is scope for deeper interest rate cuts than are expected. This would be positive for the domestic sector.

As always, risk averse investors should consider some listed property exposure for diversification purposes, but keep this moderate, as it is not a riskless asset, as was evident during the sell-off.

Evan Robins is a portfolio manager at Old Mutual Investment Group

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.