South Africa is finally getting a handle on its debt problem – the biggest drain on the government’s ability to deliver services and invest in projects that could speed up growth and create jobs.

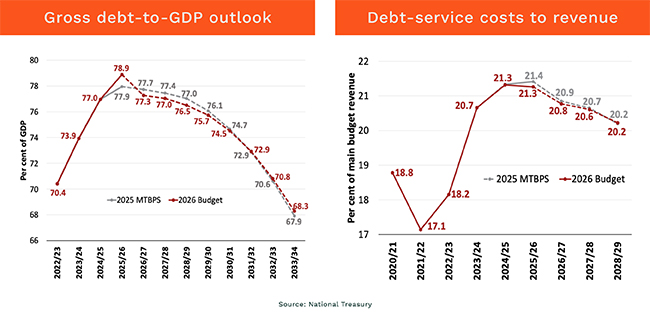

For the first time since the global financial crisis in 2008, when as a percentage of GDP it was just 25%, debt is likely to peak in the financial year to end-March, and then start falling.

“That period of rising debt has come to an end,” National Treasury director-general Duncan Pieterse wrote in the Budget Review, which gives an overview of the government’s revenue and spending plans.

But at an expected 78.9%, the level is more than the 77.4% that Treasury projected last year – mainly because of a struggling economy, and more debt in issue.

Still, the cost of servicing all our borrowings is improving, growing slower than overall expenditure for the first time this decade.

Since the global financial crisis, South Africa’s debt-service costs have surged from 9c of every rand of tax revenue to about 21c – and at R432.4bn it is the biggest line item in the budget. That’s roughly 20% more than the amount set aside for basic education (the next largest).

Scrapping new taxes

Treasury is also making progress on another front: containing spending. The primary surplus – which excludes interest expenses and serves as a barometer of the state’s ability to cut its liabilities – is expected to swell to 2.3% over the next three years, from an estimated 0.9% in the year to end-March, and 1.6% in the next.

It is the first time since the mid-2000s that the government is running a “consistent and growing” primary surplus. Much of that is due to the windfall from record high gold prices. These brought in an extra R28bn (out of total revenue of R2.13-trillion and spending of R2.67-trillion).

That has allowed Treasury to scrap R20bn of additional taxes it had planned for this budget, as well as adjust personal income tax brackets and medical tax credit by 3.4%, in line with its 2026 inflation forecast, and after two years of no adjustments.

Tax limits have also been lifted for price gains to bring relief to “assist small businesses and encourage savings”, said Treasury.

From April, the compulsory VAT registration threshold increases to R2.3m, while the tax-free investments annual limit is increased from R36,000 to R46,000.

However, the South African Revenue Service (Sars) fell R15bn short of its R120bn debt-collection target, disappointing expectations it would bring in R20bn-R50bn in additional taxes.

That’s notwithstanding the extra R7bn Sars had been given in the past year to hire 1,500 additional debt collectors.

Delays in the “onboarding” of staff, a rise in disputed debts and increases in deferred payment arrangements hindered their efforts. Sars is now collaborating better with banks and hiring more legal professionals to bring civil suits.

Lukewarm growth projections

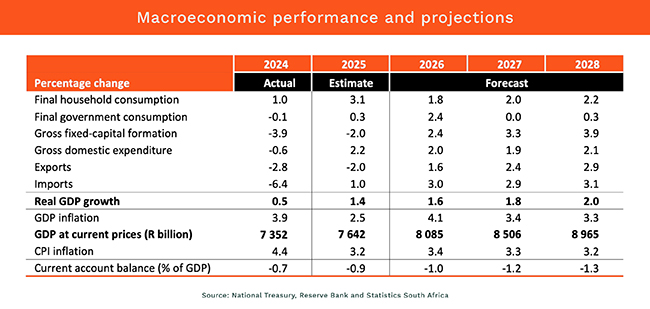

As for growth, the picture is somewhat better, with the economy expected to expand by 1.6% in 2026, compared with an estimated 1.4% last year (at the medium-term budget policy statement in November, Treasury forecast just 1.2%).

Growth could reach 2% by 2028, underpinned by household spending that will be helped by “further gains in real purchasing power, moderately stronger wage growth, falling inflation, wealth gains from rising asset prices, improved consumer sentiment and better credit conditions.” Further support will come from “continued momentum on structural reforms, improving confidence, lower interest rates and higher investment”.

Even so, “structural constraints continue to limit economic growth and investment” says Treasury.

“Growth remains well below the levels needed to meaningfully reduce unemployment and generate sufficient revenue to expand social and economic services,” it warns.

In his speech, finance minister Enoch Godongwana also blamed “persistent logistics bottlenecks, weak public infrastructure and the recent outbreak of foot-and-mouth disease” as risks to South Africa’s outlook.

“In light of this, rapid inclusive growth remains our only durable path forward,” he said, adding that “steady structural reform and responsible public finances are the bedrock of a prosperous” country.

‘Fiscal anchor’

Treasury hopes to “entrench” sustainable public finances through a “principles-led fiscal anchor”, rather than “numerical rules”, which will be developed by the ministry in consultation with the cabinet.

In a nutshell, the fiscal anchor is an obligation on every new government to show, upfront, how it plans to keep spending within its means. This, said Treasury, will “ensure that the fiscal position is sustainable”.

Asked whether political factions might derail its plans, Godongwana answered “no”.

Municipal overhaul

Arguably, the biggest drag on South Africa’s growth is its increasingly broken municipalities. As many as 162 municipalities – 63% of the total – were in financial distress in 2023/24. Here, too, Treasury has a plan.

In provinces, the government is now enforcing strict headcount controls and “compensation discipline”, including centralising HR, payroll and administration functions and tightening recruitment approvals. A clause in the 2026 Division of Revenue Bill will also allow the Treasury to “redirect infrastructure grants from local municipalities that have proven incapable of implementation to the Development Bank of Southern Africa, the Municipal Infrastructure Support Agent or capable district municipalities”.

Public sector spending will top R1-trillion over next three years, of which R577.4bn will be spent by state-owned companies and other public entities; R217.8bn by provinces; and R205.7bn by municipalities.

“The fastest-growing item of expenditure is spending on buildings and other fixed structures, which increases by 9.9% over the medium term,” said Treasury. “This reflects a deliberate shift in the composition of spending to infrastructure investment to support service delivery and economic growth.”

ALSO READ:

- Treasury lifts TFSA limit to R46,000

- 10 things to know about the budget

- Budget by the numbers: Tax relief and a break for diamond miners

Top image: Finance minister Enoch Godongwana. Picture: Gallo Images/Brenton Geach.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.