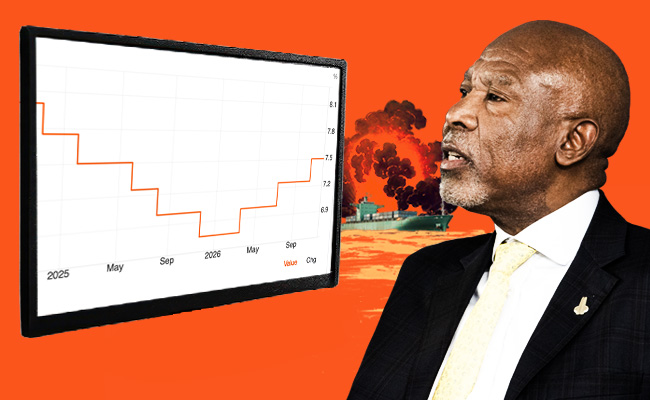

Lesetja Kganyago and his monetary policy committee may not be geopolitical experts. But that is still little solace, given the grim scenarios he has sketched of a world wedged in the centre of a lingering war in the Gulf.

In the first scenario, where the war, which broke out after the US and Israel struck Tehran on February 28, lasts another two months or so, oil averages close to $100 a barrel, the rand is about 5% weaker against the dollar and inflation rises above 4%. In that case, the South African Reserve Bank (SARB) will be called upon to hike interest rates once this year.

But in the second, more alarming, scenario, where the conflict lasts for more than a year, oil remains above $100, the rand plunges 10% to the dollar and inflation climbs above 5%. In that case, several more interest rate hikes will be called for.

Kganyago was adamant that the Bank won’t hesitate to hike rates if the spiralling economic chaos threatens South Africa’s inflation target, which was recently lowered to 3%.

“What you can’t do when you are faced with a shock is to sit and wait until inflation has risen and then only respond at that time,” Kganyago said in a question-and-answer session on Thursday, after announcing the repo rate would remain on hold, for now, at 6.75%.

While the bank’s baseline forecast now shows rates staying flatter for longer – postponing cuts it had pencilled in only two months ago – its two war scenarios point to higher borrowing costs this year if the conflict drags on.

“When we adopted the new 3% inflation target, we were clear that achieving it could take a couple of years. Until recently, conditions were favourable and it looked like we would get there fast,” Kganyago said. “Now there has been a negative shock, and it could take a bit longer. Nonetheless, all our forecasts show inflation reverting to 3% during the next two years.”

Well, depending on what happens in the Middle East, that is.

Oil prices have surged more than 40% since the US and Israel struck Iran, while the rand has weakened from below R16/$ before the attacks to above R17/$. South Africa imports almost all of its oil, so the combination of a weaker currency and higher oil prices could send fuel prices sharply higher in April.

And, worryingly, the oil shock is not the only problem consumers need to contend with: from April 1, motorists will have to absorb an extra 21c a litre in fuel taxes, as the higher general fuel levy, carbon levy and Road Accident Fund levy all take effect.

Look into shorter-term bonds

“Our base case was a hawkish hold – and this is definitely a hawkish hold,” Kristof Kruger, head of fixed-income trading at Prescient Securities, tells Currency, using central-bank parlance for a bias towards tighter interest rate policy.

He predicts at least two increases by the end of the year.

For bond investors, this could mean shifting to shorter-dated debt, such as government-issued Treasury bills or bank-issued negotiable certificates of deposit (NCDs).

“I would probably say it’s time to go into more of a money-market instrument – until there’s more clarity over the hiking path.”

Still, things can shift very quickly. “That’s markets for you – it changes in a minute,” says Kruger. “In a week’s time, it could bounce the other way again.”

Tertia Jacobs, treasury economist at Investec Corporate and Investment Bank, says her feeling “right now” is that “we’re not going to escape a rate hike, unless things pull back next month”, though the caveat is that there are many moving parts that make forecasting difficult.

While the SARB expects the oil shock to drive headline inflation to 4% in the second quarter (from an estimate in January of 3.3%), Jacobs thinks the spike could be worse. Depending on the size of the petrol-price increase, she sees inflation rising closer to 4.8% or even 4.9% in the near term, with her full-year forecast of 4% also vulnerable to upside surprises if the fuel pass-through proves stronger.

Adding to the pressure, a weighted average 7.2% increase in contributions at Discovery Health Medical Scheme, the country’s largest medical aid provider, takes effect from April and will also feed into inflation.

Limited room to hike

Still, any hiking cycle should be “shallow”, Jacobs believes.

That’s because a lot of firms will likely swallow the first-round increases in fuel and transport costs rather than pass them on immediately, she adds, especially if they think the conflict could be over within three or four months.

It means the SARB’s May meeting is potentially far more consequential. By then, it should have a clearer sense of whether the oil shock is fading or becoming more persistent.

Whatever happens in May, though, the fallout for the economy may be felt hard. While the SARB is still forecasting growth rising towards 2% over the next few years, it now says the risks to that outlook are on the downside due to the war and the oil shock.

For households and businesses hoping for a break, that is already a bleak turn. South Africa grew all of 1.1% in 2025, and Investec’s forecast of 1.5% growth this year had much to do with consumer spending holding up, on the back of more rate cuts.

Jacobs warns that higher inflation will hit disposable income directly, and she is more doubtful than the SARB that growth will continue to grind higher from here. In her view, any cyclical recovery has effectively been delayed. Worse, already-fragile business confidence could weaken again if the conflict drags on, which will knock any budding recovery in investment.

“Everything is pushed out,” Jacobs says. “What we were expecting for this year is now more like a 2027 story.”

ALSO READ:

- Smart trade for the Gulf meltdown: Don’t look

- Godongwana claims control of new 3% inflation target

- Why the debate over prime does, and doesn’t matter

Top image: Reserve Bank governor Lesetja Kganyalo. Picture: Gallo Images/Alet Pretorius; Rawpixel/Currency collage.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.