At the start, 2026 was looking quite promising. Inflation had fallen, interest rates had been cut, the government of national unity (GNU) had delivered a measure of political and fiscal stability, and consumers were finally spending again.

Then, in late February, the US and Israel struck Iran.

Within days, the Strait of Hormuz – through which roughly 20% of global oil and gas ordinarily moves – was effectively shut. Oil prices surged. The rand weakened. Fuel prices spiked.

Finally, on Friday, it looked as if talks between Iran and the US had produced a breakthrough, and Brent crude plunged as it appeared shipments would resume. Alas, it was not to be. Both sides have again resorted to war talk; some tankers and cargo ships have been fired at, with free passage again stoppered by threats of annihilation.

South Africa’s vulnerability to this oil shock is far more acute because, a few years ago, the country produced the bulk of its own refined fuel. Following the 2022 shutdown of the Sapref refinery – previously the nation’s largest – and the suspension of the Engen plant in Durban after a 2020 explosion, domestic refining capacity has roughly halved. South Africa now imports 70%-80% of its finished fuel requirements, most of it from the Middle East, with diesel accounting for the largest share. What remains is Sasol’s coal-to-liquids plant in Secunda, as well as the Natref refinery and Astron Energy in Cape Town, which has been shut down for planned maintenance since mid-February. Both of those rely on crude oil sourced primarily from West Africa (Nigeria is South Africa’s single largest supplier) and increasingly from other countries on the continent, like Angola.

It is our diesel dependency that is South Africa’s central vulnerability. “We effectively run this economy on diesel,” says Dirk Mostert, director and lead economist at PwC South Africa. “About 80% of our freight travels by road. When fuel costs rise, input costs rise across the economy, and those increases eventually get passed through to consumers.”

Cost shock

That is already visible in surcharges appearing across supply chains. FlySafair has extended its fuel surcharge to mid-August, with jet fuel having surged 70% in a single week in March. The Courier Guy has implemented a 12% surcharge on deliveries, according to News24, while Moneyweb reports that Transnet Port Terminals will introduce a fuel-linked container handling charge from May, starting at R52 per container but poised to rise further if diesel prices do.

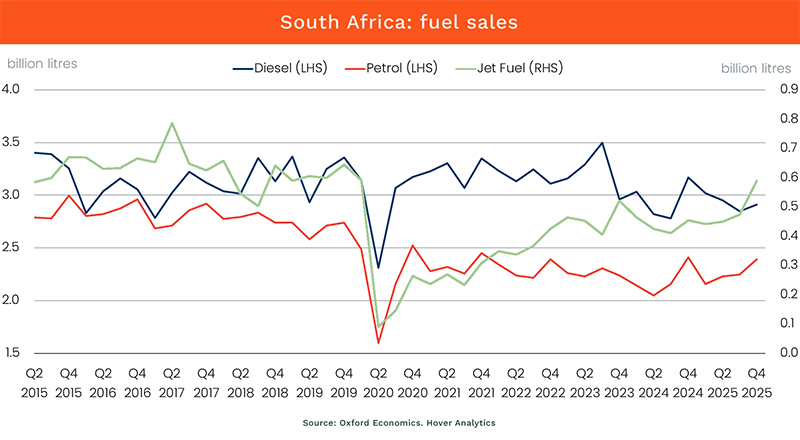

And it’s not as if prices are responding to surging demand, either. Oxford Economics analysis shows that petrol, diesel and jet fuel sales have largely plateaued since the Covid rebound and, in some cases, remain below pre-pandemic levels.

“This is not an economy overheating under strong demand,” says Jee-A van der Linde, principal economist at Oxford Economics Africa. “It is one facing a cost shock while growth remains fragile – which amplifies the impact on both inflation and output.”

As of mid-April, the Central Energy Fund, a division of the department of mineral resources and energy, was reporting under-recoveries of approximately R2.80 per litre for petrol and R8.50 for diesel, pointing to significant price increases in May regardless of how ceasefire talks progress. The government’s R3-a-litre fuel levy cut has offered some relief, at a fiscal cost of roughly R6bn for the month, but Xhanti Payi, director of Inani Strategies, says the room for further relief is narrow.

“The fuel levy isn’t something you can just keep reducing,” he says in an interview. “The bigger issue is whether this is temporary or persistent – and the global environment suggests volatility is here to stay.”

Compounding effects

No wonder Izak Odendaal describes it as “a race against time”. The chief investment strategist at Symmetry, part of the Old Mutual Group, tells Currency that “the longer the disruption continues, the greater the pressure – you start to see the possibility of central banks raising interest rates, and then effects begin to compound”.

Higher borrowing costs are one risk: the South African Reserve Bank (SARB) has already cautioned that it will act pre-emptively if it believes higher oil prices will spur inflation. In the minds of some policymakers, it’s pointless to act after the damage has already been done. Others, like Odendaal, believe the oil shock could be temporary and external, that any spike in inflation will not be demand-driven, and that monetary policy is already restrictive, so the SARB can afford to wait before hiking rates.

Be that as it may, the SARB next meets to decide on rates on May 28, when all the variables may be a little clearer. Right now, though, the threat to economic growth, not higher prices, is much more real.

Last week, the International Monetary Fund, in its latest World Economic Outlook, cut South Africa’s 2026 growth projection to just 1% from its January estimate of 1.4%, and trimmed its 2027 outlook to 1.3% from 1.5%. Disappointing, considering that the National Treasury had been aiming for 1.6% this year, rising to 1.8% in 2027 and then 2% after that.

As it is, South Africa’s GDP has hardly grown at all in 10 years, with GDP growth averaging less than 0.8% between 2015 and 2025.

Little to hold growth up

“South Africa is running out of cushions,” says Chris Hattingh, executive director at the Centre for Risk Analysis. “Over the past two years, the economy benefited from lower fuel prices, interest rate cuts, a commodity price windfall, and improved investor sentiment following the formation of the GNU.”

Those tailwinds, he tells Currency, are now reversing simultaneously because recent improvements were “not earned through structural reform. When conditions turn, there’s very little underneath to hold growth up.”

Hattingh identifies three pressure points that matter most. The first is fixed investment. Gross fixed capital formation – spending on infrastructure, factories and machinery – has been stuck between 13% and 15% of GDP for years, well below the 25%-30% range economists associate with sustained growth.

The second is energy and logistics costs – South Africa’s charges are among the highest in the world, rail networks are in ruin, and power prices have risen by about 15% a year since 2008, according to data compiled by Codera. The third is consumer spending, which has been the primary driver of recent growth, and that spending is acutely sensitive to fuel prices, electricity costs and interest rates.

George Glynos, head of research at ETM Analytics, says fixed investment in South Africa sits roughly 20 percentage points below the emerging-market average. “A realistic growth ceiling is 2%-2.5% at best,” he says. “And that’s only because of the very low base we’re coming from.”

Room to be patient

As for inflation, Van der Linde reckons the current shock isn’t as catastrophic as that seen during the early stages of the Russia-Ukraine conflict. “I see headline CPI at just over 4% for this year,” he says. “But in the next few months, we could easily end up with a 5% handle.”

South Africa’s CPI came in at exactly 3% in February. The April fuel and electricity increases alone are expected to add two to four percentage points to headline CPI before indirect effects filter through. SARB governor Lesetja Kganyago told reporters at the March monetary policy committee meeting that fuel-price growth could exceed 18% in the second quarter.

PwC’s Mostert believes the rate-cutting cycle has likely reached a premature end. “We might have expected another 25-basis point cut this year, but that now seems unlikely. For now, holding rates steady is probably the best course.”

Yet Odendaal tells Currency that the SARB should look through the shock rather than respond to it.

“This is a classic supply shock – monetary policy can’t fix that directly. Inflation was on target, and real interest rates are already positive. That gives the Bank room to be patient.”

He makes another observation that may also count in South Africa’s favour: the US dollar has not strengthened as it typically does during geopolitical stress. It barely moved during the initial shock and has since softened. “That raises interesting questions about longer-term perceptions of the dollar,” he says. “The US is increasingly a source of volatility rather than a safe anchor. It’s not a crisis – it’s a gradual margin shift – but it’s worth watching.”

For South Africa, a structurally softer dollar is not unwelcome: it provides natural support for the rand and for commodity revenues, even if it offers no protection against the underlying energy shock.

The lag effect

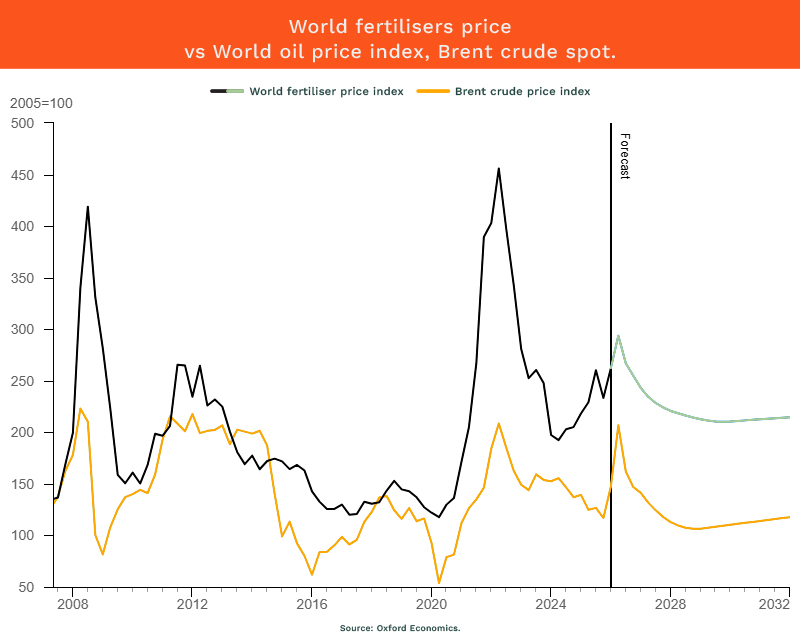

Another risk is food. Fertilisers are petrochemical products, meaning higher oil prices translate directly into higher input costs for farmers. Van der Linde of Oxford Economics Africa points to a lag effect that may only emerge later – even though South Africa has so far struck it lucky.

“Maize was planted when fuel costs were lower, but harvesting is coming up soon – that’s when you’ll see the impact,” he adds. “Winter crops like wheat are being planted now, with higher costs already embedded. If volatility persists into the second half of the year, food inflation becomes much more visible.”

An additional risk lies further out: agricultural economist Wandile Sihlobo has warned that the La Niña cycle that supported two consecutive bumper harvests is likely ending, with an El Niño – associated with drought across Southern Africa – projected for late 2026.

The combination of higher fertiliser costs and a drought season, were they to coincide, would be a compounding food security risk on top of an already stressed inflation outlook.

But, Sihlobo tells Currency, the food inflation picture is not completely bleak: a strong harvest has pushed agricultural prices lower, and that is currently absorbing some of the fuel-driven cost pressures.

“But going forward,” he warns, “that buffer disappears.”

Building buffers

The problem is that South Africa now imports more than 80% of its fertiliser, up from roughly 20% in the early 1990s, leaving the sector acutely exposed to disruption originating in the same part of the world now driving the fuel shock.

It means the September planting season is critical: if current fuel and fertiliser prices persist through to that point, farmers’ decisions about how much to plant in the summer season – which determines 2027 food supply – come into serious question.

Being a relatively small country with a small population, South Africa relies heavily on other countries to buy what we produce and to provide the capital we need for energy and infrastructure, says Payi.

“What we must do now – no matter how painful it is – is transform our energy system, reduce our reliance on crude oil, and build the right kinds of buffers. Otherwise, these problems are here to stay.”

ALSO READ:

- Phew! Relief at the fuel pumps, but rate risks linger

- What Iran’s war means for African economies

- Oil is surging. Why Sasol and Thungela are up and the JSE is down

Top image: Rawpixel/Currency collage.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.

South African government is biased they reported Israel to ICC but turning a blind eye on what has been happening to Israel from Proxies of Iran , Hezbollah Houthis Hamas they have attacking Israelis left right n center killing n kidnaping American n Jews chanting death to America n Israel

[…] in the diesel-dependent economy of South Africa. Transport costs have surged, reflected in the 70% surge in the cost of jet fuel during a single week in March. With nearly 80% of South Africa’s freight moving by road and a […]