“People always ask me what’s going to change. But what’s more important is what’s not going to change.” Jeff Bezos said that, and he was right – not just about Amazon, but about strategy itself.

Last week I was in West Africa, running a leanback session with the senior leadership team of a global heavyweight. The brief was simple: get off the dancefloor, onto the balcony, and think. No back-to-back meetings, no inbox tyranny, no activity mistaken for effectiveness. Just the kind of perspective that Ronald Heifetz and Marty Linsky – leadership scholars writing in the Harvard Business Review – argued in 2002 is not a privilege of effective leaders but an imperative of them.

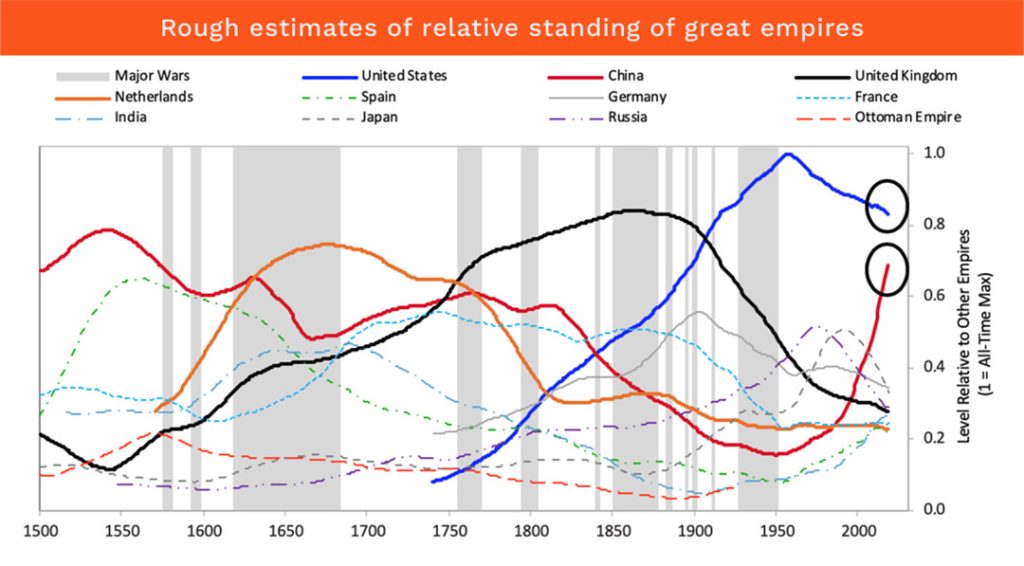

We spent time thinking about a world that has tilted noticeably on its axis. Hyper-globalisation ran hard from 1990 to roughly 2015, connecting countries, capital and people across every previous tension. Then something shifted. Brexit was the opening move, but the instinct behind it – that you do better behind walls than across them – has spread. Nationalism has risen across Europe. Trade architecture is fracturing. The US, in relative terms, has been in gradual power decline since its peak around 1960, even as China’s hockey stick climbs and India’s demographic engine begins to fire.

Ray Dalio, the hedge fund manager and historian of empire cycles, mapped this across five centuries in Principles: A Ray Dalio Company: the pattern of rise and decline is consistent, and we are somewhere in the middle of a very large transition.

In that room, the question wasn’t whether the world is changing. That argument was settled before we sat down. The question was: what doesn’t change? What are the constants a business can actually navigate by?

Three things, I argued, have held across industries, geographies, and time.

Economic context

The first is that economic context is the single biggest driver of business performance. Across the roughly 2,000 largest companies in the world, half of revenue growth and half of earnings growth is statistically explained by the economic growth rate of the country in which business is done.

Granger causality tests confirm the direction runs from country to company, not the reverse. This is not a trivial finding: it means that a great deal of what executives attribute to strategy is actually luck, and a great deal of what they attribute to bad luck is actually a structural growth shortfall. The behavioural economics literature calls this attribution bias. The implication is not passivity. Rather, if growth is the tide, then where you swim matters enormously.

Sixty-five years, 160 countries, same data

The second constant is that economic growth itself is driven by six things that have not changed in 65 years of data across 160 countries. Savings and investment at above 25% of GDP – without a single exception in the record. Demography, because babies are both future workforce and future customers. Policies and institutions, where stability of policy matters more than the direction of any single policy. Education and health, the latter carrying a higher weight than the former because you cannot educate a sick workforce. And openness – trade, capital, information, people – which can be a winner or a wrecker depending on whether the terms are truly mutual.

These six factors allow us to heat-map the world, and the picture that emerges is consistent: the centre of economic gravity is drifting south and east, and the clusters of dark green on that map sit in West Africa, East Africa and Southeast Asia.

Agility and absorption

The third constant is what separates the truly skilled businesses from the merely lucky ones. In a study of 20,000 companies over 40 years, using Monte Carlo simulation to control for fortune rather than just admire performance, fewer than 0.7% of businesses turn out to be genuinely extraordinary. What they share is not industry, geography, age, or size. What they share is a combination of two attributes: agility and absorption.

Agility is the capacity to move – to take lots of small bets, build innovation into everyday operations, treat capital allocation as a competitive weapon, and run lean hierarchies that let intelligence flow from the bottom up.

Absorption is the foundation that makes movement possible without collapse – customer centricity, fat balance sheets, stable leadership, and a culture that behaves counter-cyclically when everyone else is panicking. The businesses that sit in the agile-absorptive quadrant at once deliver growth, margins and valuations that are materially and persistently superior to everything else in the dataset.

Seizing the opportunities

The conversation in that room kept returning to one provocation I put on the table: Africa is not a place. It is 54 countries, each with its own institutions, growth structure, language corridor and risk profile. And the resident opportunities are material.

For the sake of an example, the continent currently represents roughly 2% of global logistics revenue against 18% of world population. That gap is not a mystery – it is an opportunity, and it will not wait indefinitely. The decisions being made now in pharma, FMCG and automotive – sectors where switching costs are high and relationships lock in for a decade – are closing windows that take years to reopen.

The right response to a world that resists forecasting is not to stop thinking about the future. It is to ask better questions about it. Not “what will change?” but “what will stay the same?” Not “where are we winning?” but “where are we under-indexed against the growth that is already structural and already under way?” The three constants don’t tell you what the future looks like. They tell you what to build towards, regardless of what arrives.

That is strategy. Everything else is just a busy calendar.

Adrian Saville is a professor of economics, finance and strategy at Gibs, and a founding director of the Centre for African Management and Markets, as well as the founder of Boundless World. This story was first published on his Substack.

ALSO READ:

- Investing in Africa: from uncertainty to opportunity

- How Capitec’s ‘seven dwarfs’ built a banking behemoth

- Africa – finally boom adjacent

Top image: Rawpixel; Currency.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.