It was 2021, and Mexican billionaire Ricardo Salinas Pliego was at the peak of his wealth. With an estimated fortune of $15.9bn, he stood among Latin America’s richest men. But a single deal that year, involving a little-known financier and a web of shell companies, would erase nearly 60% of his net worth and force him to delist Grupo Elektra, the business he had built on his grandfather’s legacy.

Sixty-nine-year-old Salinas – a towering figure in Mexico’s business world – alleges that he was the target of an elaborate cross-border fraud that deprived him of Grupo Elektra shares worth about $400m, or the equivalent of about 3.4% of his grandfather’s company, one of Mexico’s largest appliance retailers and the owner of Banco Azteca, one the country’s top banks by branches and depositors.

The man at the centre of the alleged scheme is Ukrainian-born Vladimir “Val” Sklarov, a convicted fraudster who was sentenced to a year in prison in the US in the late 1990s.

Now, Grupo Salinas is pursuing legal action across three continents in an attempt to recoup its shares and losses. It has approached the UK High Court, and filed criminal referrals in the US. In Mexico, regulators have launched a review of Elektra trading activity.

As part of the alleged scam, Sklarov’s lawyer and longtime associate appears to have secretly routed Salinas’s funds into luxury real estate deals across the US and Europe, according to property records. Those included $6.45m for a New York penthouse with views over Central Park, $2.67m for a Virginia mansion bought in the name of his lawyer, and a $6m French château registered under the name of Sklarov’s wife. In Greece, two villas in the wealthy suburbs of Marousi and Ekali completed the portfolio.

In total, more than $22m worth of real estate was purchased between July 2021, when the deal was signed, and July 2024, when it legally collapsed.

DWF Law, Sklarov’s legal representatives in the UK, did not respond to requests for comment.

The alleged con

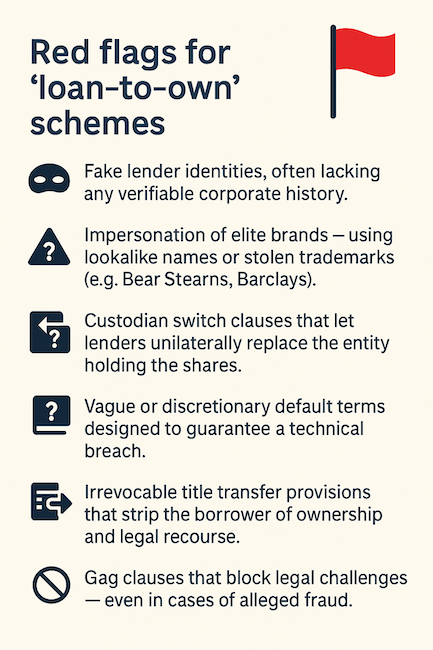

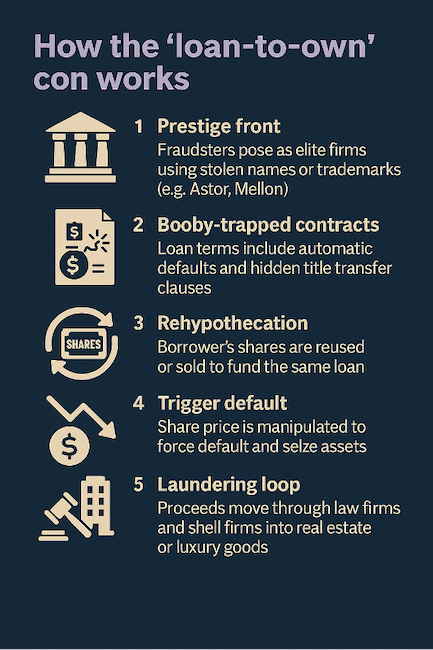

According to UK and US court filings, Sklarov orchestrated what financial crime experts call a “loan-to-own” con: a share-backed loan agreement that appears legitimate but is designed to trigger a default and demand a margin call – a legal demand that Salinas provide more shares or cash to top up the losses.

The court documents reveal that in 2021, Salinas transferred roughly 7.2 million Grupo Elektra shares as collateral to a lender known as Astor Asset Management. He was led to believe that Astor was a Pittsburgh-based private financial firm linked to the Mellon family and run by its CEO, Thomas Mellon.

But according to the UK High Court, Mellon was a fictitious persona (used to evoke the prestige of the founder of Mellon Bank), and the company he allegedly ran existed largely on paper. The judge found that Astor and its supposed leadership were fabrications created to give the deal a veneer of legitimacy.

Salinas was assured he would retain beneficial ownership of the shares, which would only be sold if he defaulted on the $110m loan. Within weeks of the deal, however, and without his knowledge, nearly 1 million shares were transferred to a Bahamian custodian called Weiser Global Capital Markets – an entity allegedly linked to other supposed frauds involving Sklarov.

Rather than holding the shares in trust, Weiser and Sklarov’s other affiliates began selling them. The proceeds were allegedly used to fund the very loan Salinas asked for, though Astor claimed they rehypothecated the shares – a practice in which collateral is used to raise further funds. In reality, they sold it, which meant a change in the owner’s identity.

According to court filings, Sklarov admitted that more than $360m in proceeds from Elektra share sales flowed through Astor-linked accounts. At least $64.5m in loans were then issued to Salinas – not from the lender’s capital, but from the unauthorised sale of his own collateral, the shares.

Intentional design

Salinas’s legal team alleges that the transaction was designed from the outset to induce default. The loan agreement included discretionary triggers that would classify Salinas as being in breach of the terms, gag clauses that prevented legal redress, and transfer provisions that gave Astor the right to liquidate the collateral without arbitration or court oversight.

Once the shares were out of Salinas’s control, they were systematically sold through large brokers including Morgan Stanley, BBVA and Merrill Lynch, according to trading logs reviewed by Salinas’s team.

As the shares were dumped in the market, the price dropped – by more than 40% between July 2021 and July 2024. This price fall triggered technical thresholds under the loan agreement, allowing Astor to declare a breach and seize further shares.

According to Eduardo Salceda, vice-president of financial investments at Grupo Salinas, the parent company could see volume fluctuations in the clearinghouse data but was blocked from identifying the ultimate sellers. Foreign-held shares were managed by Citibanamex, a Mexican bank, which declined to disclose ownership details, even to the central depository, Indeval.

Two intermediaries appear to have been instrumental in brokering the deal. The first was Alexandre Torti, a senior executive at Fininvest, which was later acquired by the Swiss wealth manager Octogone Group. He was a longtime adviser to Salinas’s family office and helped arrange the loan.

The second was Zara Akbar, a securities adviser at Jersey-based Ennes Global. She introduced Astor to Torti on behalf of Ennes, who vouched for its legitimacy. Akbar has denied wrongdoing, saying through a spokesperson that she acted in good faith based on the documents available at the time.

Fininvest and Octogone are not defendants in the case. Torti has denied any wrongdoing.

“We trusted what we were told by Astor and Torti, who assured us the contract was being honoured,” Salceda said in an interview via Zoom. In his testimony, he alleges that Torti did not forward certain email chains to him at the time.

Alarm bells start ringing

By October 2021, new ownership records showed that beneficial control of Salinas’s pledged shares had changed. Another offshore custodian, Monaco-based Tavira, was brought in – again by Astor.

Tavira later refused to confirm whether it still held more than 6 million Elektra shares, instead stating that the burden of proof lay with Salinas. Weiser, meanwhile, said it could trace only $12m in transactions and was unable to provide further information.

By mid-2024, the damage was done. Elektra shares had plunged by more than 70% since the deal was struck three years earlier, with more than $4bn in lost market capitalisation. Grupo Salinas moved to delist Elektra from public trading and filed for legal relief in multiple jurisdictions.

In August 2024, the UK High Court granted an interim worldwide freezing order against Sklarov and his associates, blocking them from moving or selling assets linked to the Elektra deal. Sklarov tried and failed to overturn the order.

To follow the funds, Salinas’s lawyers also filed a petition in the US District Court for the Southern District of New York. Their goal was to access documents and bank records held by American financial institutions that may have facilitated the movement of money tied to the alleged fraud.

The filings reveal that from April 2022 to July 2024, Sklarov’s US-based lawyer and longtime associate, Jaitegh “JT” Singh, moved more than $271m through so-called interest on lawyer trust accounts at JPMorgan Chase. These accounts are typically used to hold client money securely. Instead, they allegedly became conduits for laundering funds.

Singh’s trust accounts allegedly transferred more than $150m to more than 15 companies associated with Sklarov, including Vanderbilt Capital, Sierra Universal Corp and America 2030 Capital Ltd.

More than $32m went directly to Sklarov’s children over three years. On a single day in July 2024, $60m moved through Singh’s accounts.

Singh did not respond to requests for comment. An email to his law firm bounced back.

Singh’s law firm and its affiliated entity, Jurist IQ Corp, appear to have functioned as financial gateways, helping funnel proceeds from stock sales into layered trust structures and shell companies.

Property records show that by 2024, Sklarov and his network had acquired more than a dozen luxury properties, worth over $22m.

Patterns and playbooks

This is not the first time Sklarov has faced legal scrutiny. In a separate 2024 case, also filed in the US District Court for the Southern District of New York, titled Chenming Holdings (Hong Kong) Limited vs Val Sklarov, et al, similar tactics were alleged: fraudulent loan agreements, stock-backed collateral, and laundering via Singh’s trust accounts. The same shell companies, such as Vanderbilt and Astor, reappeared.

What makes “loan-to-own” schemes so potent is the use of legal camouflage. Sklarov and his associates allegedly exploited features designed to protect investors – such as trusts, custodians, and attorney-client privilege – to conceal the fraud.

While Sklarov maintains that the transactions were legal, alleging that Elektra’s share price fell due to internal issues and not manipulation, his asset disclosures remain under scrutiny. Court documents show he failed to list dozens of properties and companies linked to the alleged scheme.

‘Engineered forfeiture’

By July 2024, trading in Elektra shares had been halted at the request of Grupo Salinas. When trading resumed in early December, the stock plummeted 71% in a single day – erasing $5.5bn from Salinas’s net worth. (The share price has since staged a partial recovery as the company heads towards going private.)

Today, Salinas today has a net worth of $6.9bn. Still, it’s enough to keep him in the top 500 on Bloomberg’s Billionaires Index. And his family remains in control of 75% of Elektra.

But for him, the courtroom battles are about more than recovering his wealth. They are an attempt to expose how legal and financial tools can be weaponised to execute corporate heists behind a curtain of respectability.

In the words of one insider familiar with the case: it was “an engineered forfeiture – structured so the borrower could never win”.

This version updates the second and fifth paragraphs under the subheadline “The alleged con’” for clarity and to include more detail on how the “loan-to-own” scheme operated, including confirmation that the shares were sold. It also corrects the paragraph under “Alarm bells start ringing” to remove an earlier reference suggesting Tavira was brought in without Salinas’s consent.

Top image: Mexican businessman Ricardo Salinas Pliego. Picture: Tomas Cuesta/Getty Images.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.