For most people, the answer to financial stress feels obvious: earn more money. It is a neat, intuitive solution. If you are struggling, you assume the problem is income. If you are doing well, you assume it is because you earn enough.

The data suggests there’s much more to it than that.

South Africa’s inaugural Franc wealth index, a large survey of financial wellbeing, finds that what people do with their money matters far more than how much they earn – giving individuals a glimmer of hope in that, while they don’t have agency over the level of their income, they do over how they use it.

Conducted by Franc, a South African fintech offering digital financial advice and access to investment and savings products, the survey polled nearly 4,000 financially active South Africans, with a majority of working-age adults between 26 and 45, and 62% female.

The results show that consistent behaviours such as saving, budgeting and investing make someone two to three times more likely to achieve a high wealth index score than someone with a higher income, more education or more years of life experience.

“Financial wellbeing is often invisible until it becomes a problem,” says Thomas Brennan, Franc’s co-founder and CEO. “And, like health, people feel the symptoms without knowing the underlying cause.”

Unlike traditional measures that focus on net worth or asset values, the Franc wealth index is a behavioural composite. It scores individuals out of 100 based on the frequency and quality of actions such as maintaining an emergency fund, managing debt and diversifying investments. By separating these habits from static factors like age or income, the index aims to measure a person’s financial trajectory rather than their current position.

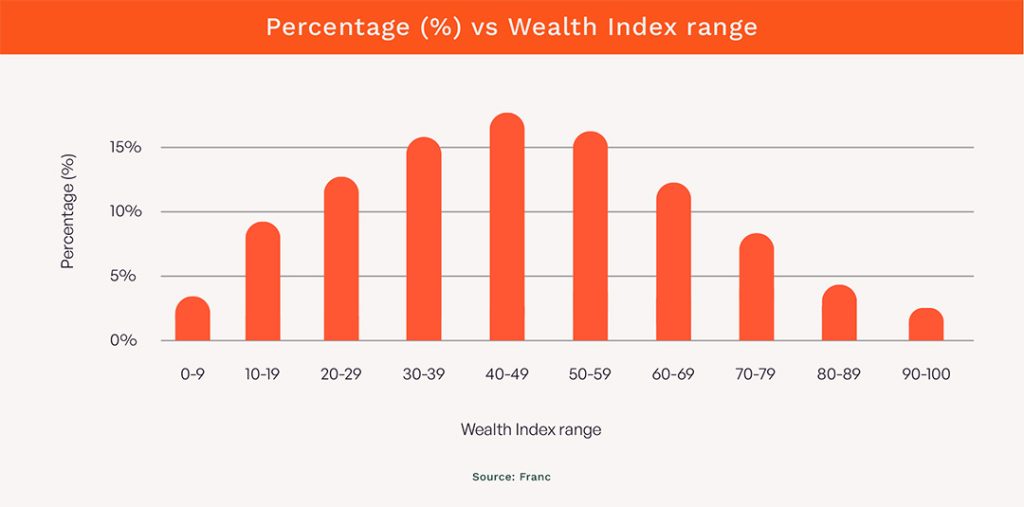

It evaluates respondents across three pillars: resilience (debt management and emergency savings), growth (investing and retirement planning), and mindset (financial knowledge and confidence). In its inaugural 2026 reading, the national wealth index score is 45 out of 100, with 58% of respondents scoring below 50 – suggesting that most financially active South Africans lack the core habits associated with long-term wealth formation.

The data shows that while higher income improves outcomes, certain behaviours have a stronger effect. Respondents who invested using automated, diversified strategies were significantly more likely to achieve high scores than those who simply earned more.

This is also evident in gender outcomes. Female respondents recorded a slightly higher average wealth index score of 52, compared with 50 for men, and were more likely to fall into higher-scoring categories. The data suggests more consistent financial behaviours within this group, despite well-documented income disparities.

Among the behaviours tracked, having a clear and regularly reviewed financial plan stands out. Respondents with defined goals were far more likely to save and invest consistently.

“What you do with your money is a more powerful predictor of financial health than your age, education, or income,” the report concludes.

The illusion of ‘more’

Of course, higher income does improve outcomes – but only up to a point. Wealth index scores rise steadily as earnings increase, but then plateau and even dip slightly among top earners. Beyond a certain level, more money does not automatically translate into better financial wellbeing.

Within the same income bracket, the gap between top and bottom performers can be as wide as 50 points on the index. These are people earning similar salaries, yet living very different financial lives.

According to the South African Reserve Bank Quarterly Bulletin released in March, the household saving rate has slipped into negative territory, reaching -1.4% of disposable income in the fourth quarter of 2025. At the same time, household debt edged higher to 61.8% of disposable income. It means much of any income gain is absorbed by consumption or debt servicing.

The two-pot retirement system, introduced in September 2024 to give members access to a portion of their retirement savings, reflects the same pressure. According to Today’s Trustee, 62% of Momentum FundsAtWork members making claims at the start of the 2026 tax year were doing so for the third time in just three tax windows, with the vast majority withdrawing the full amount available.

Alexforbes says it has paid more than R3.6bn in tax on behalf of members accessing their savings. Even with withdrawals taxed at marginal rates, immediate liquidity needs appear to be outweighing longer-term considerations.

The real fault lines

Two factors dominate: debt and the absence of emergency savings.

A third of respondents are overindebted. This group’s median wealth index score is 31, compared with 53 for those managing debt effectively. That 22-point gap marks the difference between relative stability and financial distress.

Emergency savings tell a similar story. Eighty-seven percent of respondents do not have enough savings to cover three months of expenses. Those without a buffer are less likely to invest, more likely to carry debt, and significantly more anxious about their finances. As the report notes, these are “the fault lines through which financial wellbeing fractures”.

This pressure is visible in the broader credit market. According to Eighty20 and Xpert Decision Systems, 26-million South Africans are managing a combined loan balance of R2.7-trillion, with one in three loans in arrears.

Within the Franc data, 34% of respondents carry high debt burdens, with repayments consuming more than 35% of income.

Knowledge isn’t the problem

Nearly two-thirds of respondents rate their investment knowledge as intermediate or above, and 78% report having financial goals – though more than half have no concrete plan to reach them.

Yet this knowledge does not translate into outcomes. People understand what they should do – save regularly, invest consistently, plan for retirement – but they struggle to act on it.

“What is missing is the structural foundation that turns good intentions into compounding progress towards financial stability and wealth,” the report notes. The problem is not information. It is execution.

The anxiety paradox

Income is a relatively weak predictor of financial anxiety, accounting for only 18% of what the data calls the “calm score”. What matters far more is liquidity – specifically, whether you have accessible savings. In fact, moving from no emergency savings to even one to three months’ cover has three times the impact on reducing anxiety as receiving a 20% salary increase.

“Stability is felt not in how much you make, but in how much money you can access in case of emergency,” the report states.

Without a buffer, even a high income can feel precarious. With one, even a modest income can feel manageable.

Habits that matter

The report identifies a set of “keystone habits” – actions that have a disproportionate impact on financial outcomes. At the top of the list is having a clear, regularly reviewed financial plan, which is associated with improvements across saving, investing and debt management.

Other high-impact behaviours include:

- Investing regularly, particularly through automated, diversified strategies;

- Saving consistently each month; and

- Building and maintaining an emergency fund.

Many South Africans are, as the report puts it, “caught between awareness and action” – engaged with their finances, but lacking the habits to turn that engagement into progress. Financial wellbeing is less about a single breakthrough moment than a series of small, repeated decisions.

The path to financial stability is not a mystery – and doesn’t begin with a higher income. What it requires is consistency.

ALSO READ:

- A practical guide to prioritising your money

- The power of simple money habits

- South Africans are taking home 47% less than a decade ago – the ugly truth

Top image: Rawpixel/Currency collage.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.

Please guys, well-being is not one word, it is hyphenated: well-being.

Mark! We at Currency LOVE a grammar stickler and, as it turns out, we have one working for us in the shape of Shirley de Villiers. You don’t want to get on the wrong side of Shirley’s style guide 🙂

Which is a very long-winded way of saying: wellbeing is, in fact, the English usage of the word. Well-being being the American form. So: we are both right. Cheers, Giulietta

Yes, and a good riposte!